India's D2C Brands Built Empires Online. Now They're Betting on Malls | Why They're Opening Physical Stores

💡 InsightsIndia's D2C brands built on digital are now opening physical stores at scale. Rising online ad costs, low e-commerce penetration at 8%, and stronger in-store conversion rates are driving the shift. Founders from Snitch, Gargi, IGP, Eume, Traya, and more share why offline is now central to growth.

A decade ago, India's most exciting consumer brands were built entirely online. They bypassed the high street, cut overhead costs, sold directly through websites and apps, and grew quickly. The promise of the direct-to-consumer, or D2C, model was simple: remove the middleman, protect margins, and build a loyal audience through digital advertising.

Today, many of those same brands are signing mall leases. Lenskart operates over 2,270 stores across India. Nykaa has crossed 237 stores in 79 cities. Snitch, which opened its first physical store less than two years ago, reached 100 stores by the end of 2025. The Bear House opened its first store in Bengaluru in March 2025 and expanded to seven cities within months.

This is not a retreat from the original model. It is a rethink. India's D2C brands are finding that physical stores can work as customer acquisition channels, trust-building tools, and conversion engines, in some cases, more efficiently than digital advertising.

What is D2C and Why Does it Matter?

D2C, or direct-to-consumer, refers to brands that sell products directly to the end customer, without going through distributors, wholesalers, or large retail chains. A founder could launch a website, run social media ads, and ship from a warehouse without negotiating shelf space or giving customer data to a marketplace.

Between 2018 and 2022, India saw a sharp rise in D2C launches across beauty, fashion, pet food, and home furnishings. By 2025, India had over 800 active D2C brands in a market estimated at $15 to $20 billion, projected to reach $100 billion by 2030. But growth came with a problem: most brands were competing for the same pool of online shoppers, on the same platforms, at rising costs. That pressure is what has pushed many of them towards stores.

The Scale of the Shift

The data from property consultants tells the story clearly. According to CBRE's report on India's D2C retail landscape, D2C brands leased approximately 5.95 lakh square feet of retail space in the first half of 2025 alone, 18% of total retail leasing activity across India in that period, up from 8% in the first half of 2024. D2C brands more than doubled their share of India's retail leasing within a single year.

Fashion and apparel led the way, accounting for over 60% of the space leased, followed by home furnishings, jewellery, and health and personal care. These categories share a common trait: consumers typically prefer to see, touch, or try products before buying.

The store counts of major brands reflect the same trend. Lenskart operates 2,270-plus stores across 431 cities, with plans to add more than 450 new locations in FY26. Nykaa has 237 stores across 79 cities. Bluestone has over 270 stores. Snitch went from zero to 100 stores in roughly 18 months. Accessories brand Joker & Witch opened its first store at Lulu Mall in Bengaluru and is actively expanding, targeting 10 to 20 store openings in 2026 with the goal of generating 50% of its revenue from offline sales.

Rising Online Acquisition Costs

The biggest factor pushing D2C brands offline is the rising cost of finding new customers online. Industry data and founder accounts confirm that customer acquisition costs on Meta and Google have risen sharply, with estimates putting the year-on-year increase at 25 to 40% for Indian D2C brands. The period of cheap digital reach effectively ended around 2022, with Meta CPMs rising significantly since 2023 as more brands competed for the same pool of online shoppers.

By comparison, stores, particularly in Tier 2 cities, where rents are lower, and competition for attention is less intense, can work out considerably cheaper on a per-customer basis. Lenskart has disclosed that its average customer acquisition cost runs at approximately INR 850 per new customer, with its Tier 2 stores producing better unit economics than metro locations, owing to lower rents and higher volumes of first-time buyers.

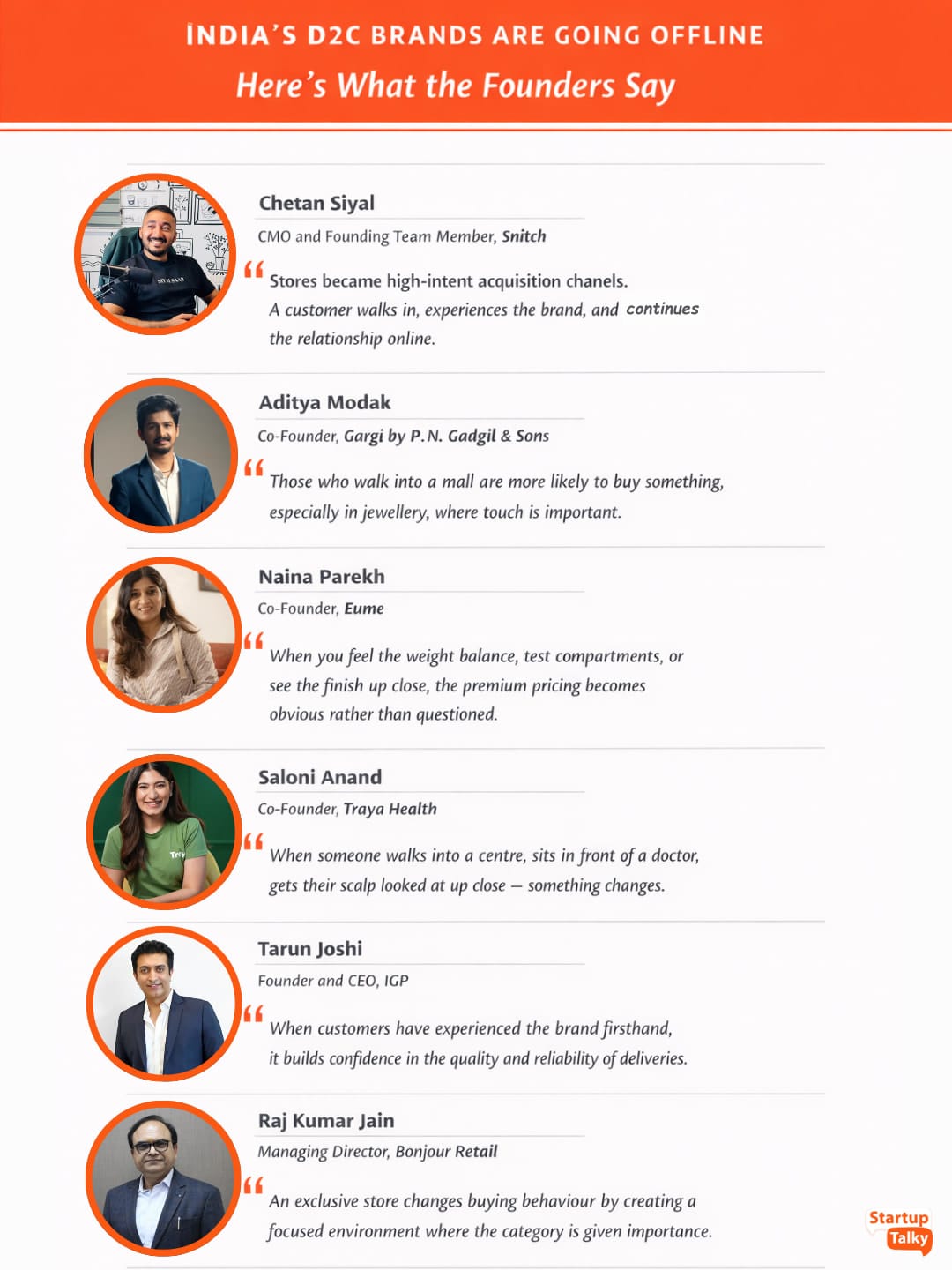

For Chetan Siyal, CMO and Founding Team Member of Snitch, the move offline was never about escaping rising digital costs. "It was never defensive," he says. "Yes, CAC was going up, but retail for us was an offensive bet from day one. India is still a 90-plus % offline market, especially in fashion, where touch, fit, and instant gratification matter."

What stores unlocked for Snitch, Siyal says, was a different kind of growth logic altogether. "Stores became high-intent acquisition channels. A customer walks in, experiences the brand, and then continues the relationship online. So instead of thinking CAC versus rent, we started thinking in terms of blended customer acquisition and lifetime value across channels. That's when the maths started making a lot more sense."

Trust, Returns, and Conversion

For categories where fit, shade, or texture matters, online retail has a built-in problem: high return rates. Physical stores reduce this by letting customers experience the product before buying, which leads to fewer returns, higher satisfaction, and better repeat purchasing.

Nykaa's leadership has described physical retail as essential for the beauty category, particularly for products such as foundation, where colour-matching on screen is unreliable.

Snitch's stores report conversion rates of 50 to 60%, more than half of everyone who walks in makes a purchase. That compares with low single-digit conversion rates typical of e-commerce. The brand has also reported that average order values in stores are nearly double those on its online platform.

The pattern holds in other categories, too. Aditya Modak, Co-Founder of Gargi by P.N. Gadgil & Sons, which has scaled 15 times in three years using a kiosk-led model, says offline conversions in jewellery are generally two to three times higher than digital leads. "Instagram leads are mostly about finding new things," he explains. "They help people become aware of and consider your brand, but they usually need to interact several times before they buy. Those who walk into a mall are more likely to buy something, especially in jewellery, where touch is important."

Naina Parekh, co-founder of luggage brand Eume, makes a similar point about premium products. "A physical store allows customers to experience the craftsmanship, materials, and design details firsthand, which a screen simply cannot replicate," she says. "When you feel the weight balance, test compartments, or see the finish up close, the premium pricing becomes obvious rather than questioned." Parekh adds that the in-person experience has also significantly reduced Eume's return rates, as customers make more confident decisions when they have physically handled the product.

The Store as Acquisition Channel

The most important shift in thinking for D2C brands is this: a store is not an overhead cost. It is a place where new customers are won, and in many cases, the most cost-effective place to do so.

Siyal describes how the opening of Snitch's physical stores changed the brand's entire marketing structure, allowing it to spread spending across channels. The stores also changed how customers move between touchpoints. "A lot of customers discover us in-store and then transact online later. Equally, a lot discover online and convert in-store. It's a two-way street now. We don't look at channels in isolation anymore. It's one brand, multiple touchpoints."

This coming together of online discovery and offline conversion plays out differently by category and market. For Gargi by P.N. Gadgil & Sons, the kiosk model, smaller than a full store, positioned in high-footfall mall locations, has proved particularly well-suited to fashion jewellery, a category often driven by impulse. "Kiosks offer visibility, accessibility, and a low-pressure browsing experience," Modak says, adding that the format's unit economics make it easier to scale than large flagship stores.

| Earlier D2C | Now |

|---|---|

| Online-only | Omnichannel |

| Performance-led growth | Experience-led growth |

| Low touchpoints | Physical + digital touchpoints |

| Rising CAC (digital-heavy) | Blended CAC (online + offline) |

| Transactions-focused | Relationship-driven |

The Offline Market's Size

There is a basic reality that many D2C brands have overlooked for too long. According to data from PCMI and the India Brand Equity Foundation, e-commerce accounts for roughly 8% of total retail sales in India in 2024. Even by 2030, that figure is expected to reach only around 10%.

The remaining 90 to 92% of Indian retail spending happens in physical stores. India's total retail market is expected to grow from $1 trillion in 2024 to $2 trillion by 2030. A brand competing only for the digital slice is, by definition, limiting how much of that market it can reach.

This matters most outside India's major cities. Tier 2 and Tier 3 markets have growing consumer demand but lower trust in online transactions and less reliable delivery infrastructure.

Raj Kumar Jain, Managing Director of Bonjour Retail, India's largest socks and hosiery brand, which has been in the market since 1988 and sells through over 7,000 multi-brand outlet partners, has found that physical stores serve a purpose beyond simply selling. "An exclusive store changes buying behaviour by creating a focused environment where the category is given importance," he says. "Customers get the opportunity to explore different options, understand product features, and make more informed choices." For a category like socks, typically treated as an impulse or add-on purchase in multi-brand retail, a dedicated store changes the customer's relationship with the brand entirely.

Modak echoes this for Tier 2 and Tier 3 markets specifically. "Trust is very important in these markets, particularly when it comes to buying jewellery. Physical locations give customers the chance to see and feel the product, which builds confidence and reduces doubt."

| Metric | E-Commerce | Offline Retail |

|---|---|---|

| % of Total Sales | 6–8% | 92–94% |

| Consumer Habit | Growing | Established |

| Ideal For Try Before Buy | Low | High |

New Models: Dark Stores and Experience Centres

Not every offline move looks like a traditional retail store. Tarun Joshi, Founder and CEO of gifting brand IGP, has built a network of over 100 dark stores across 29 cities, small fulfilment hubs that allow the brand to deliver gifts within 30 to 60 minutes. "Hyper-local infrastructure is a game-changer right now because it lets us deliver fast and efficiently," Joshi says. The dark stores use predictive analytics to plan inventory by PIN code, occasion, and festival calendar.

But Joshi sees physical experience centres as a separate and complementary layer. IGP has opened retail stores in Mumbai and Gurugram, which function as extensions of the online platform. Customers can browse in-store and access a wider range through tech-enabled ordering.

"When customers have experienced the brand firsthand, it builds confidence in the quality and reliability of deliveries, even when the recipient is in another city," he says.

IGP's current approach is to open one offline experience store for every ten dark stores.

Trust in Health and Wellness

The shift to physical is not limited to fashion and lifestyle brands. Saloni Anand, Co-founder of hair care brand Traya Health, says that for a health-focused product, a clinic is a fundamentally different type of customer touchpoint. "When someone walks into a centre, sits in front of a doctor, gets their scalp looked at up close, and hears exactly what is going on and what we are going to do about it, something changes," she says.

Traya began as a digital-first brand and opened its first clinic in Pune before expanding to 18 centres across India. Anand says customers acquired through the clinics show stronger long-term behaviour.

"They have had a face-to-face consultation, seen the clinical setup and the diagnostic tools. That starting point is different from someone who clicked an ad online. Higher trust at entry means better adherence to the treatment plan, less drop-off, and stronger retention."

She also notes that the offline and online experiences are designed to feed into each other, not operate separately. A customer who starts online and later visits a clinic does not start from scratch, the doctor already has their hair test results, treatment history, and progress. "The system is the same. The centres simply add a layer of clinical depth and personal reassurance on top of it."

Challenges in Going Offline

The shift to physical retail is not without real difficulty. D2C brands entering the offline world face operational and structural challenges that digital experience does not prepare them for.

Mall operators have historically been reluctant to give prime space to digital-first brands without a proven offline track record. The general view in the industry is that a significant funding milestone changes how mall operators engage, with well-funded brands finding it considerably easier to secure premium locations than those without a strong financial backing.

Running a physical store is also fundamentally different from managing a website. Merchandise must be refreshed regularly, visual presentation requires constant attention, staff must be trained, and inventory must be managed across both channels at once. Keeping a store feeling fresh is a genuine operational challenge. Online, a new collection goes live instantly with a catalogue update. Offline, it requires physical merchandise changes, consistent visual presentation, and careful supply chain coordination, making it far more demanding to manage.

Smaller D2C brands without strong funding face an additional barrier: prime retail locations remain largely out of reach. Mall operators typically favour established tenants or well-funded brands, creating a two-tier situation where capital-rich D2C brands get premium spots while smaller ones are pushed to lower-footfall locations.

What the Shift Signals

The D2C move into physical retail reflects a broader rethink of how consumer brands in India grow. The brands doing well are building joined-up systems, where a customer discovers a brand on social media, looks it up online, visits a store to try the product, and completes the purchase through whichever channel suits them best.

Malls, after years of caution around digital-first tenants, are increasingly open to D2C brands, particularly in beauty, fashion, and wellness, as tenants that bring footfall and energy.

The Tier 2 and Tier 3 opportunities remain largely untapped. According to Bain research, 60% of new e-commerce shoppers since 2020 have come from Tier 3 or smaller cities. Stores in these markets, as Lenskart's own data shows, can match metro-level revenues at lower rents.

For D2C founders in India today, the question has shifted. It is no longer a question of whether to build a physical presence. It is how quickly to do so, and where to open first.