Samajhdaar Ko Ishaara: The Real Reason Ankur Warikoo Shut Down His Course Business

An investigation into what one of India's biggest creators isn't saying about his ₹100 crore "shutdown."

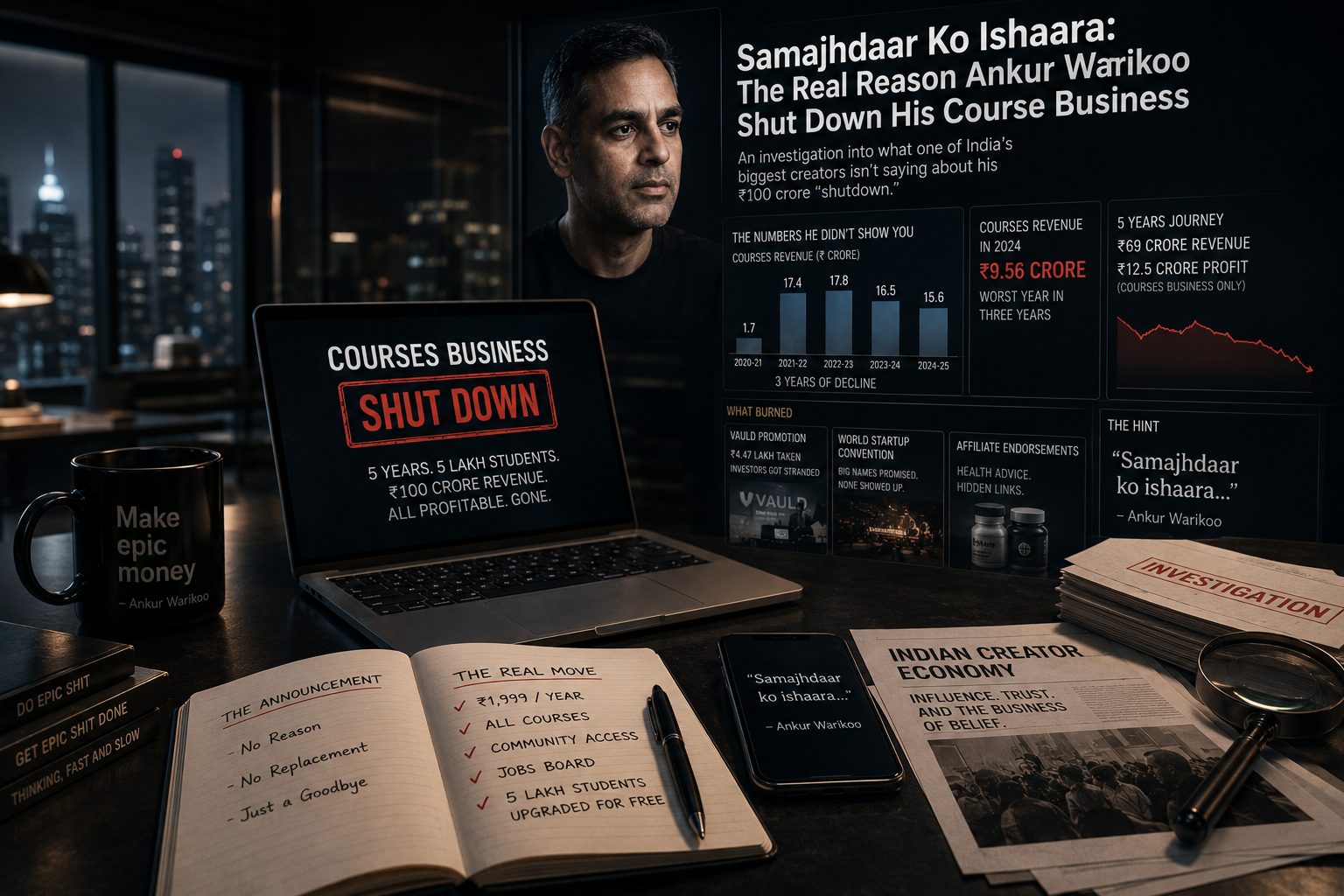

On the evening of Friday, May 15, 2026, Ankur Warikoo posted a video. Forty-five seconds, shot in his usual half-formal, half-confessional style. He was shutting down his courses business. Five years. Five lakh students. A hundred crore in revenue. All profitable. Gone.

No reason. No replacement. No next step. Just a goodbye, dressed up as a teaser.

The internet did what the internet does. By Saturday morning, a thousand reply guys were either canonizing him as a visionary or eulogizing him as a fraud. The smart ones did the only honest thing: they waited.

Twenty-four hours later, the actual move arrived. The courses weren't dead. They had been "converted into a subscription." Nineteen hundred and ninety-nine rupees a year. All courses, present and future. Community access. A jobs board. Five lakh existing students upgraded for free. The cost of a single old course now bought you everything.

This was framed as a moral pivot. "Between making more money and helping more people, the choice was super clear to me." A line so polished it could have been engraved on a brass plaque.

But underneath the announcement, in the replies to his own post, a follower asked the obvious question: is a recession driving this?

Warikoo replied with one Hindi line: "Samajhdaar ko ishaara…"

A hint to the wise.

That hint is where this story actually begins.

Part One: The Numbers He Didn't Show You

A hundred crore is the kind of number that ends conversations. You hear it, you nod, you move on. Which is exactly what it's designed for.

Here is what is actually true, drawn from his own disclosures and India's public corporate filings.

The legal entity that runs WebVeda is called Zaan WebVeda Private Limited. It was incorporated in 2011 by Ankur Warikoo and his wife Ruchi, sat dormant for nine years, then got repurposed in 2020 as a courses business. Over the five years that followed, the entity took in roughly sixty-nine crore rupees in total revenue. Not a hundred. The "₹100 crore" number includes books, speaking fees, and brand collaborations bundled together and presented as if they were all course revenue.

The courses-only piece, by his own admission on Twitter in January 2025, was ₹9.56 crore in calendar 2024. He called it, in the same post, "the worst year in three years." For a business he just told the country was a hundred-crore juggernaut, that is a strange thing to say.

The annual revenue trajectory of the entity tells a clean story:

- 2020-21: ₹1.7 crore (launch year)

- 2021-22: ₹17.4 crore (the COVID explosion)

- 2022-23: ₹17.8 crore (the peak)

- 2023-24: ₹16.5 crore (the first slip)

- 2024-25: ₹15.6 crore (the third year of decline)

This is not the financial profile of a business at its peak. This is the financial profile of a business that is being harvested for cash while it slowly fades. Notice that profit margins actually expanded during the decline, from thirteen percent to nineteen percent. That isn't growth. That's cost-cutting faster than revenue falls. In the finance world that move has a name. It's called managed decline.

And cumulative profit across the entire five years comes to roughly twelve and a half crore. Not twenty-five. The bigger number, like the bigger revenue number, includes everything Warikoo ever earned through that entity, which is a fair definition of his "business" only if you accept that the books he wrote, the keynotes he gave, and the Instagram reels he posted for paying brands all count as "the course business."

He knows this. So do his accountants.

Part Two: What Burned

If you've followed Indian finance Twitter for more than a few years, you remember Vauld.

In October 2021, Warikoo posted a YouTube video describing Vauld as a kind of crypto fixed deposit. Park your money, earn twelve percent. He took ₹4.47 lakh for the promotion. He has confirmed this number on the record. He has also said he had thirty lakh of his own money parked in Vauld, which he framed at the time as having "skin in the game."

In July 2022, Vauld froze withdrawals. Roughly eight lakh Indian retail investors got stranded. Many of them were students and first-jobbers who had taken his advice about putting "stable" crypto into a "safer" product. Some lost up to a lakh and a half rupees each. Warikoo's defense was that he too had money stuck, that Vauld hadn't shut down but "ceased operations," and that the money wasn't lost, just frozen. It is a defense that nobody in the affected community has ever quite forgiven him for.

Six months later, in March 2023, he was part of the promotional rollout for an event in Noida called the World Startup Convention. The poster promised Elon Musk, Sundar Pichai, Nitin Gadkari, nine thousand angel investors, and fifteen hundred VCs. Founders paid up to ten lakh rupees for booths. None of those people showed up. The organizers vanished with the money. Warikoo's defense was that he wasn't involved in conceptualizing or organizing the event. He had only done a single Instagram collab reel.

Three months after that, he tweeted weight-loss advice with affiliate links to whey and omega-3 supplements. Dr. Abby Philips, the hepatologist who goes by The Liver Doc, ran him over publicly. His defense, again, was that he wasn't really endorsing them, despite the literal disclaimer on his post that said he earned an affiliate income from purchases through those links.

Then Ashneer Grover, on stage at IMT Ghaziabad in March 2023, was asked by a student to compare himself to Warikoo. Grover's response is on YouTube. "You can abuse my mother and sister, I won't say a thing. But don't compare me to Ankur Warikoo." Then he walked off the stage.

In August 2023, Warikoo tweeted a joke about Prithvi Shaw's mother saying he looked thin. Shaw lost his mother as a child. The internet remembered. Reddit, in particular, remembered.

None of these incidents, individually, are career-ending. Cumulatively, they did something more dangerous. They drained the brand of the one currency a personal-brand business runs on. Trust.

By early 2025, the most-upvoted Reddit thread about him on r/personalfinanceindia read like a eulogy: "Influenzas have a shelf-life. His is over, as simple as that. He marketed shady firms like Vauld and got so many gullible folks loose money. Now I barely see anybody on this sub or on other finance subs who follow him."

Five hundred and thirteen upvotes. No counter-thread defending him got close.

Part Three: The Quiet Letter From SEBI

While all this was happening, something else was moving in the background. Slower. Less visible. And ultimately far more consequential than any Reddit thread.

On January 29, 2025, the Securities and Exchange Board of India issued a circular with the catchy name SEBI/HO/MIRSD/MIRSD-PoD-1/P/CIR/2025/11. It is the most important document in this entire story, and almost no one in India's mainstream business press has connected it to Warikoo's shutdown.

Here is what it does, in plain English.

If you are a SEBI-regulated entity in India, which includes every broker (Zerodha, Groww, Angel One, Upstox), every mutual fund house, every Asset Management Company, every Registered Investment Adviser, every distributor, every research analyst, you are now legally barred from any direct or indirect monetary relationship with an unregistered finfluencer. That word "indirect" is doing a lot of work. You can't route a payment through an agency. You can't run a "marketing partnership." You can't do an affiliate deal. You can't even buy ads on a podcast where the host pumps your product.

Ankur Warikoo is not SEBI-registered. He has confirmed this himself, in an interview with The Ken that was later cited in legal commentary. His defense, made before the circular existed, was that mandatory registration shouldn't apply unless an advisee directly pays an adviser. The January 29 circular made that argument moot.

This matters because of who Warikoo's brand partners have been. He has demonstrably promoted Smallcase. He has done tutorial videos for Tickertape. He has co-promoted IndMoney and Zerodha together in branded reels. He is an investor in Wint Wealth and has featured them. He has done sponsored content for the mutual-fund-adjacent universe for years.

Every single one of those brands, as of January 29, 2025, is legally prohibited from paying him another rupee for promotion.

If you're a creator earning ₹2.76 crore a year from "brand collaborations" (which is what Warikoo himself disclosed for calendar 2024), and the entire premium tier of that universe just got cut off, what do you do?

You'd start by pivoting your content out of finance, quietly, before anyone notices. Look at his "warikoo careers" channel from late 2025 onward. The recent video titles include things like "4 STEPS to Get a Job in 2026 When AI is Taking Over" and "26 AI Prompts That Will CHANGE Your Life" and "Why Gen Z is STRUGGLING in their CAREER." Careers. AI. Productivity. Layoffs. Everything safely outside SEBI's perimeter. The shift is visible if you look for it.

You'd also add a quiet new disclaimer to your remaining finance videos, the one that now reads: "We are not SEBI-registered investment advisors or analysts. Any paid promotions, sponsorships, or brand collaborations featured in this video will be clearly disclosed." That is not the voice of a confident creator. That is the voice of a person who has talked to a lawyer.

And you'd watch what SEBI does to the people who don't pivot fast enough.

In February 2025, SEBI banned a finfluencer who called herself the "She-Wolf of Dalal Street," Asmita Patel. The order impounded ₹53.67 crore from her. The most striking detail in the order was that Patel had earned only $13,700 from actually trading the markets she claimed expertise in. She had earned $11.4 million from selling courses about trading.

In December 2025, SEBI came for Avadhut Sathe. The order impounded ₹546 crore. Sathe ran a trading academy. He didn't recommend specific stocks. He taught what he called methodology. SEBI said it didn't matter. The model itself was the problem.

When the regulator signs an order impounding more than half a billion rupees from a finance educator who never told anyone which stock to buy, the message to every unregistered finfluencer in India is clear. The perimeter has moved. You are now inside it.

This is the wider context in which Warikoo's "Samajhdaar ko ishaara" lands.

He cannot publicly say "SEBI killed my brand-deal pipeline and I'm operationally vulnerable because I never registered." Saying it would invite the regulator to look backwards at his Smallcase and Tickertape and IndMoney promos and decide whether any of them require disgorgement. So he says something cryptic in Hindi, lets the audience interpret it as a comment on the macro economy, and moves on.

Smart people read the room differently.

Part Four: Why Nineteen Hundred and Ninety-Nine

Once you understand what's getting amputated, the pricing of the subscription stops being a feel-good democratization story and starts looking like cold math.

If you needed to replace ₹9.56 crore of course revenue at ₹1,999 a year, you'd need about 47,800 paying subscribers. If you wanted to replace the entire ₹15.6 crore annual entity revenue, you'd need about 78,000. Across his combined social reach of roughly fifteen million people, that's a conversion rate of about half a percent. The industry benchmark for free-to-paid in newsletter subscriptions is two to five percent. He needs to hit a fraction of that.

The math, in other words, works comfortably. But the price reveals strategy.

A creator launching from strength prices up. A premium repositioning. Akshat Shrivastava, who came out of INSEAD and BCG, charges ₹12,537 a year for his Wisdom Hatch community and ₹25,000 for his NRI tier. Sharan Hegde's 1% Club is ₹16,999 lifetime. The Ken, which is sub-only journalism, is ₹3,245. The Morning Context was historically ₹1,999. That ₹1,999 isn't a creator-economy price point. It's a sub-only journalism price point. Warikoo took the floor.

He went low because he had to. Because the math at ₹4,999 would have required convincing a smaller, pickier audience that the courses were worth premium money, exactly the conversation he can't have after years of refund complaints and 99consumer's 2.0/5 rating on his catalogue. Going to ₹1,999 sidesteps the value debate entirely. The pitch becomes "you used to pay this for one course; now you get everything."

The other tactical decisions are clever in ways that get glossed over.

Annual billing only. No monthly tier. Indian subscription churn at the monthly tier runs five to eight percent a month, which compounds to brutal annual numbers. Annual billing locks in cash up front and hides churn in a way that protects optics for at least twelve months.

Five lakh alumni grandfathered free for year one. This sounds generous. It's actually the smartest cold-start of any Indian creator move in recent memory. Even a ten percent renewal at ₹1,999 in year two equals ₹10 crore, which by itself replaces the courses-only revenue line. Free year one is the conversion funnel, not a charity.

Hosting on his own webveda.com, not on Substack or Patreon. Substack has structurally failed for Indian creators because of Stripe limitations and the RBI's 2021 e-mandate rules around international recurring payments. Warikoo runs his own payment rails domestically, almost certainly through Razorpay. He looked at where every other Indian Substacker has died and went the other way. That's good operating.

And finally, the valuation arithmetic. One-time course revenue is treated as transactional and trades at roughly one to two times revenue in any future M&A. Subscription revenue trades at five to ten times annual recurring revenue. If he hits a hundred thousand paying subscribers, he has roughly twenty crore of ARR, which a private buyer could plausibly value at one to two hundred crore. Which is, of course, the same hundred-crore number he's been claiming all along. Now it would actually be defensible.

So when he says "between making more money and helping more people, the choice was super clear to me," what's true is that he's chosen both. The subscription model very likely makes him more money over time on a smaller base. It also lets him sound like a saint while doing it. These are not in tension. They never were.

Part Five: The Industry He's Running From

The Warikoo story is also a snapshot of a sector. Indian edtech, the entire category, is on fire.

BYJU's defaulted on a $1.2 billion term loan in early 2024 and went into Chapter 11. The founder is facing a $1.07 billion default judgment. HSBC values Prosus's stake in the company at zero. The Android app got delisted in May 2025 because of unpaid AWS bills.

Unacademy has cut nearly two thousand jobs since 2022, revenue is bleeding, and the company is being forced back into offline coaching after the pure-online subscription model failed at scale. PhysicsWallah is the exception, and the only reason PhysicsWallah is the exception is that it priced itself dramatically below the market and went after low-income test prep, which Warikoo is structurally not going to do.

Edtech funding in India crashed eighty-seven percent from its 2021 peak. Strip out PhysicsWallah and 2024 funding fell roughly seventy-five percent year on year. More than two thousand edtech startups have shut down between 2020 and 2024.

Course completion rates have collapsed below five percent industry-wide. Refund rates on premium courses run between twenty-one and twenty-eight percent. Customer acquisition costs for course creators have quadrupled in two years.

This is not a category where you launch a confident new pivot. This is a category from which you retreat strategically, hopefully before everyone else figures out you're retreating.

Warikoo's pivot is genuinely early relative to other Indian creators. Most of them haven't moved at all. Aman Dhattarwal is still doing per-course on Apni Kaksha. Pushkar Raj Thakur is still doing launches. Khan Sir is still doing a freemium app plus offline coaching. The only direct precedent for what Warikoo just did at his scale is Sharan Hegde's 1% Club, which is genuinely impressive, but which also laid off fifteen percent of staff in late 2024 with the public taking a certain amount of pleasure in the irony. The model can hit eighty crore in ARR. It can also break operationally if the operator overhires on the optimism.

If Warikoo executes well, he becomes the case study. If he doesn't, he becomes the cautionary tale. There isn't a middle outcome.

Part Six: The Real Story

Here is the version of this story that the headlines didn't tell you.

Ankur Warikoo's courses business was in a three-year revenue decline. The brand-deal stream that supplemented it has just been legally cut off by SEBI's January 2025 circular, because he never registered as an investment adviser. The category around him is collapsing. The audience trust is corroded by Vauld and Noida and the supplement promotions. AI is commoditizing personal-finance and productivity content faster than any creator can adapt to. The Substack model that works for global creators is structurally broken in India because of payment rails.

He picked the only available move. Convert the courses to an all-you-can-eat subscription priced at the floor, lock everyone into annual billing, grandfather the alumni base for free to seed cold-start, host on his own platform to dodge the payment-rail trap, pivot content gently out of finance into the SEBI-safe zones of AI and careers and productivity, and dress the entire thing up as a values-driven decision to "help more people."

It is a smart move. It is well-timed. It is well-priced. It may even succeed at the new model and end up generating a more durable business than the one it replaced.

But it is not the story that was told.

The story that was told was "I built a hundred-crore profitable business and I'm shutting it down because the system is broken." The actual story is "the system was breaking me, and the system around me, and the only way out was to consolidate what I had into something the regulator can't touch and the AI can't replace, and I needed a narrative that wouldn't make any of that obvious."

That cryptic line he posted, in Hindi, in reply to a stranger's question on Twitter, may end up being the most honest sentence in the entire announcement.

A hint to the wise.

A Final Note on What to Watch

There are two numbers nobody outside his team will see for another eighteen months that will tell you whether this worked.

The first is the year-two renewal rate on the five lakh grandfathered alumni. Anything below ten percent and the model is in trouble. Above twenty and he's running away with it.

The second is what shows up on his next public income disclosure. If the brand-collaborations line falls dramatically from ₹2.76 crore, the SEBI thesis confirms itself. If it holds, he found a workaround.

Until then, all anyone has is what he chose to say, and what he chose not to.

Samajhdaar, as the man said, ko ishaara hi kaafi hai.

A hint, for the wise, is enough.

If you found this useful, the underlying research came from his own public disclosures, MCA filings of Zaan WebVeda Private Limited, SEBI's January 29 2025 circular and subsequent enforcement orders, the Storyboard18 reporting on finfluencer brand-deal collapse, and roughly thirty cross-checked sources on Reddit, X, Indian business press, and YouTube. Want the source list? Just ask.