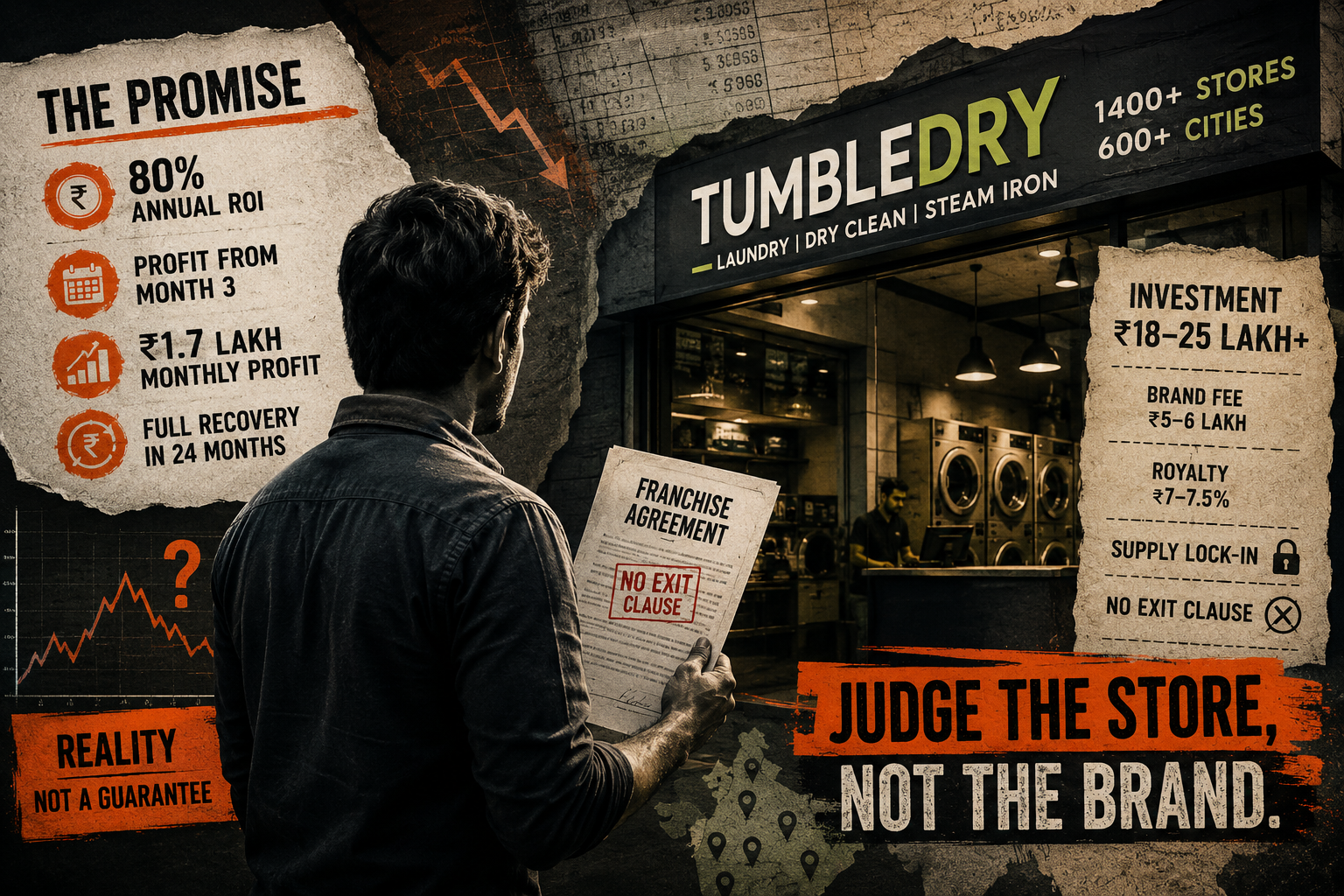

Tumbledry Is Profitable. That Does Not Mean Your Tumbledry Store Will Be.

Tumbledry markets its laundry franchise on an 80% annual return and profit from the third month. The company itself is real, bootstrapped and profitable. But a profitable franchisor is not the same as a profitable franchise.A pre-investment reality check.

If you have ₹25 lakh and an entrepreneurial itch, you have probably seen the pitch. Tumbledry, India's largest organised-laundry chain, sells its franchise on numbers that are hard to ignore: an 80% annual ROI, profit from the third month, ₹1.7 lakh a month, and full investment recovered in 24 months.

Here is the first thing to understand, and the most important. The company behind those claims is genuinely profitable. That tells you almost nothing about whether your store will be. A franchisor and its franchisees make money in different ways, and confusing the two is the costliest mistake a prospective franchisee can make.

The franchise at a glance

| Company | Tumbledry Solutions Pvt Ltd (incorporated 2019, bootstrapped) |

| Scale claimed | 1,400+ stores across 600+ cities (early 2026) |

| Total investment | ₹18–25 lakh (location and model-tier dependent), plus working capital and rent deposit |

| Franchise / brand fee | ~₹5–6 lakh one-time (reported; not officially disclosed) |

| Royalty | ~7–7.5% of revenue (reported; sources range 5–7.5%) |

| Store size | 250–500 sq ft |

| Exclusive territory | ~10,000 households per store |

| Agreement | 3 years, renewable |

| FY25 financials | Revenue ₹98.8 Cr, net profit ₹1.9 Cr (third straight profitable year) |

Figures compiled from MCA/Tracxn filings, franchise databases and franchisee accounts; "reported" items are not officially published by Tumbledry.

The company is real, and it is profitable

Start with what is solid, because plenty about this category is not. Tumbledry is not a scam. It is a real, operating business, bootstrapped to over 1,400 stores without a rupee of outside investment, covered by credible editorial press (The Hindu, YourStory), partnered with LG and Electrolux for equipment, and a recipient of a genuine international industry award from CINET, the Netherlands-based textile-care body.

Its financials, verified through Tracxn filings, are healthy:

| Financial year | Revenue | Net profit |

|---|---|---|

| FY21 | ₹7.2 Cr | −₹1.2 Cr |

| FY22 | ₹16.6 Cr | −₹1.5 Cr |

| FY23 | ₹65.1 Cr | ₹2.6 Cr |

| FY24 | ₹94.7 Cr | ₹3.6 Cr |

| FY25 | ₹98.8 Cr | ₹1.9 Cr |

The company has been profitable for three straight years and carries very little debt. FY25 net profit did fall about 47% from the year before, on thin net margins of roughly 2%, but the business is growing and financially sound. If you are evaluating whether the brand will still exist in five years, the answer is reassuring.

Why the franchisor's profit is not your profit

Now the catch, and it is the single most useful idea in this entire piece.

A bootstrapped franchisor like Tumbledry earns its money primarily from two things: the fees it charges franchisees, and the margin on the supplies it sells them. Every new store pays a brand fee, a running royalty, and is required to buy its chemicals and machinery through the company. That means the franchisor can be very profitable because it is signing up franchisees, regardless of how those individual outlets perform.

A healthy franchisor and a healthy franchise are different things. The parent's books tell you the brand is alive. They tell you nothing about whether a single store makes money.

So when a sales pitch points to the company's growth and profitability as proof that you will succeed, it is answering a question you did not ask. The only evidence that matters for your decision is store-level profit and loss from real, operating outlets in locations like yours. Never the parent company's financials.

The claims, against the evidence

Tumbledry's marketing numbers are best treated as ceilings, not expectations. India has no Franchise Disclosure Document requirement, so none of these figures is independently audited.

| Marketing claim | What the evidence actually shows |

|---|---|

| 80% annual ROI | Self-reported, unaudited. No third-party basis exists. |

| Profit from month 3 ("95% of stores") | This means cash-positive on operations, not capital recovered. Franchise databases cite 14–16 months to break even. |

| Full recovery in 24 months | Real franchisees report 2+ years, and some imply a far longer 5–6 year horizon once ramp-up is included. |

| ₹1.7 lakh monthly profit | No store-level P&L has ever been published. Aggregator sites simply echo the company's own figure. |

A conservative model makes the gap concrete. At 20 customers a day and a ₹400 average ticket, a store grosses about ₹2.4 lakh a month. After royalty, staff, rent and chemicals, net profit is more likely ₹1–1.2 lakh a month, which puts payback on a ₹25 lakh investment at roughly 20–25 months, not three. The optimistic ₹1.7 lakh figure assumes 35-plus customers a day, consistently, from month three. Whether your specific location can deliver that is the whole question.

The structural risks worth diligencing

Beyond the optimistic numbers, three features of the model carry real, structural risk. These are drawn from franchisee accounts on Reddit, Quora and MouthShut, so treat them as reports to verify, not settled facts. (Complaints also skew negative by nature; satisfied owners rarely post.)

1. The no-exit clause. This is the most serious. A franchisee in Bangalore, posting on r/LegalAdviceIndia in 2025, said she had invested ₹40 lakh and was told the franchise could not be cancelled: if she stopped operating, she would forfeit the full amount, leaving resale at a possible loss as her only way out. A franchise you cannot exit is an illiquid asset, and if your circumstances change, you are stuck. The exit and termination clauses in the actual agreement are the first thing a lawyer should read.

2. Supply lock-in. Franchisees say they are contractually barred from sourcing their own chemicals and machinery; everything routes through Tumbledry. As one franchisee put it on Quora, "the company made us sign contracts to not use chemicals and machines of our own choice." Some rationalise this as quality control. The problem is the undisclosed markup: if the company raises input prices mid-term, your margins shrink with no recourse, and the price list is not public. Get it in writing before signing.

3. The ₹50,000 enquiry deposit. In at least two documented cases, a MouthShut reviewer and an Instagram exposé, prospects who paid a refundable ₹50,000 deposit said it was withheld after they decided not to proceed. One wrote they had "been waiting for our money for the last 6 weeks." Two cases is not a mass pattern, but it is a yellow flag on commercial conduct. Get the refund terms, with timelines, in writing before you pay anything.

There is also territory saturation: Delhi is reportedly full, with no new franchises available, so metro applicants should confirm their location is open and check how close the nearest existing store is.

The other side

Selection bias cuts both ways, and there are credible positives. Several long-term franchisees report genuine success: one with prior business experience said his "investment is already fully recovered"; another who left a corporate job for a Noida store described himself as very happy. The company built a Manpower Training Academy that addressed the early staffing problems, and at least one prospective franchisee noted Tumbledry was the only brand that gave him contact details of existing franchisees to verify independently, which is an unusually transparent gesture if standard.

One caveat on the most accessible source of feedback: Tumbledry's Quora reviews show unusually uniform upvote counts, a pattern that suggests possible coordinated posting. Weight Quora positives accordingly, and rely on people you contact yourself.

If you are still interested: the checklist

The under-regulated Indian franchise sector puts the entire burden of diligence on you. Before signing:

- Have a franchise lawyer read the actual agreement, specifically the exit/termination clause, royalty escalation, renewal terms, and who owns your customer list if you leave.

- Get the supply price list in writing (chemicals, packaging, machinery) and compare it to open-market prices. The lock-in is contractual; the markup is what costs you.

- Speak to at least five current franchisees yourself, from a list you source independently, and ask each for real monthly revenue, net margin after royalty, and actual break-even timeline.

- Demand store-level P&Ls from three live outlets, not the company's projections and not the parent's accounts.

- Confirm territory availability for your exact location, and get the ₹50,000 deposit refund terms in writing first.

The verdict

Tumbledry is a mixed bag, leaning cautious for first-time investors. It is a legitimate, profitable brand riding a real tailwind, as organised laundry is a genuine unmet need in urban India, and some franchisees do make money. But the marketing numbers are aggressive and unaudited, the no-exit clause is a serious trap, and the supply lock-in removes your control over costs.

It can make sense for someone with time to run it hands-on for the first year or two, liquid reserves beyond the ₹25 lakh, and a verified, under-served location. It is the wrong choice for anyone seeking passive income, investing borrowed or retirement money, or operating in a saturated metro.

The one rule that survives all the noise: judge the store, not the brand. A franchisor's healthy books are the easiest thing to show you and the least relevant to your outcome. The number that decides your future is the net margin of a real Tumbledry store in a place like yours, and that is the number nobody volunteers. Make them.

If you have information related to this story, reach out through StartupTalky's tips line. Anonymity is the default.