E-Invoice Limit Under GST: Who Needs It and What Applies in 2026

The GST e-invoice limit is INR 5 crore in annual sales, and it looks at past years, not just the current one. If your sales crossed INR 5 crore in any year since FY 2017-18, e-invoicing applies to you now, even if this year's sales are lower. Here is what that means for your business.

The e-invoice limit under GST in 2026 is INR 5 crore in annual sales. Any GST-registered business whose sales crossed INR 5 crore in any financial year from FY 2017-18 onwards must generate e-invoices for all B2B transactions, exports, and supplies to government entities. The INR 5 crore limit has not changed since August 2023, and no reduction has been announced for 2026.

Two things about this rule catch most businesses off guard. First, it looks at past years, not just the current one. If your sales crossed INR 5 crore in FY 2022-23 but dropped to INR 4 crore in FY 2024-25, e-invoicing still applies to you right now. Second, if your business has GST registrations in multiple states, all of them are added together at the PAN level. A business with INR 3 crore sales in Maharashtra and INR 3 crore in Delhi has combined sales of INR 6 crore and must comply.

What Is the E-Invoice Limit Under GST?

INR 5 crore in aggregate annual sales across all GST registrations under the same PAN, in any financial year from FY 2017-18 onwards. Cross that figure once, and e-invoicing applies to you from the next financial year, permanently.

If your sales crossed INR 5 crore for the first time in FY 2025-26, e-invoicing becomes mandatory from FY 2026-27. You cannot wait to see if the current year stays above the limit.

How the Limit Has Dropped Since 2020

E-invoicing started in October 2020 for businesses with sales above INR 500 crore. The government brought it down in steps.

There has been discussion about lowering it to INR 3 crore or INR 2 crore. As of June 2026, no notification has been issued. Businesses with annual sales of INR 5 crore are better off getting set up early than scrambling after a notification drops.

Who Has to Generate E-Invoices

E-invoicing applies to all GST-registered businesses with aggregate annual sales above INR 5 crore, for these types of transactions:

- B2B sales (sales to other GST-registered buyers)

- Sales to government entities (B2G)

- Exports of goods and services

- Supplies to SEZ developers

- Credit notes and debit notes linked to the above

It does not apply to:

- B2C invoices (sales to end consumers without GST registration)

- Nil-rated and GST-exempt supplies

- Businesses in the following categories, regardless of their sales figure: banks, NBFCs, insurance companies, Goods Transport Agencies, passenger transport operators, SEZ units (as suppliers), and businesses providing admission to cinema on multiplex screens

One thing service businesses often get wrong: e-invoicing is not limited to goods. A consulting firm, IT company, or logistics provider with B2B clients and annual sales above INR 5 crore must generate e-invoices.

The Multi-State Business Rule

This is where many businesses underestimate their own applicability.

Sales are calculated at the PAN level, not at the individual GSTIN level. If you have branches in three states, each with a separate GSTIN, their sales are added together. If the combined figure crosses INR 5 crore in any financial year, all your GSTINs must generate e-invoices for qualifying transactions.

Say your Delhi GSTIN had sales of INR 2.5 crore and your Bengaluru GSTIN had sales of INR 3 crore in FY 2023-24. Combined, that is INR 5.5 crore. E-invoicing applies to both registrations from FY 2024-25 onwards, even though neither branch individually crossed the limit.

The 30-Day Rule for Larger Businesses

For businesses with annual sales above INR 10 crore, there is an additional rule. From April 1, 2025, every invoice must be reported to the Invoice Registration Portal (IRP) within 30 days of the invoice date. The IRP will reject any invoice older than 30 days. No exceptions, no late uploads.

This means invoices cannot be batched and uploaded at month-end. The invoice must be sent to the IRP on the day it is raised, or within 30 days at most. GST billing software that connects to the IRP via API handles this automatically at the point of invoice creation. This rule also applies to credit notes and debit notes, not just sales invoices.

For businesses with annual sales between INR 5 crore and INR 10 crore, the 30-day restriction does not currently apply. Generating the IRN at the time of raising the invoice is still a good practice.

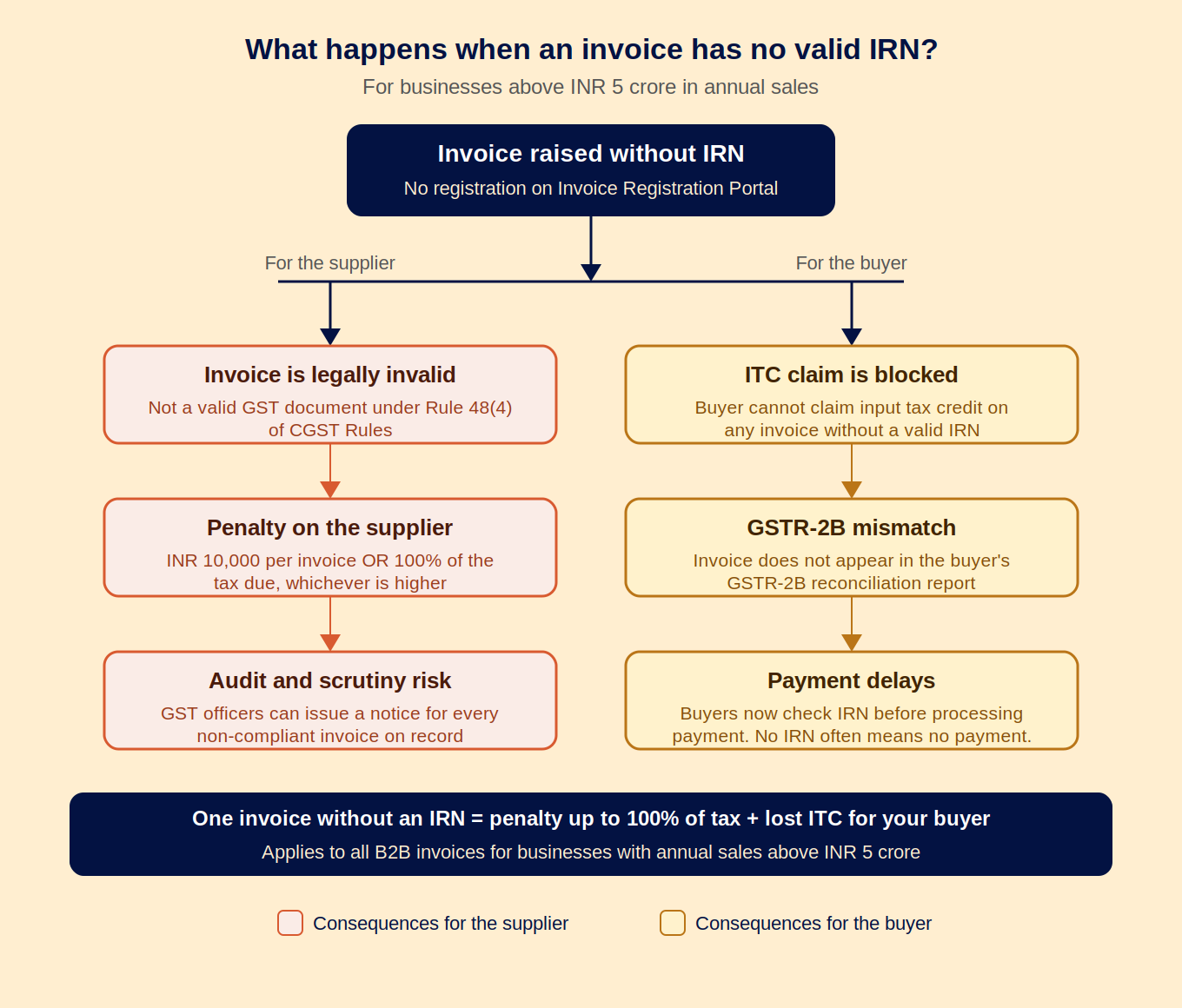

What Happens Without an IRN

An invoice without a valid IRN is not a legal GST document. Two things follow from that:

- The buyer cannot claim input tax credit on that invoice. ITC is often large for B2B buyers, and losing it on a supplier's non-compliance is a real commercial problem. Buyers increasingly check IRN validity before processing payments.

- The supplier faces a penalty of INR 10,000 per invoice or 100% of the tax amount on that invoice, whichever is higher.

How to Check If E-Invoicing Applies to You

The GST portal has a built-in check. Log in to the GST portal, go to Services, then User Services, and select "Search e-Invoice Enablement Status." Enter your GSTIN. The system will tell you whether e-invoicing is enabled and mandatory for your registration. Most GST invoicing software will check your applicability status automatically and flag it within the product.

If you have multiple GSTINs under the same PAN, check each one separately. The result can differ by registration depending on the transaction types each GSTIN handles.

E-Invoicing Exemption Declaration

If your business falls into an exempt category (banking, insurance, GTA, and so on), the GST portal has an "E-Invoice Exemption Declaration" feature. Filing this declaration avoids automated compliance notices that the portal sends to businesses above INR 5 crore that are not generating IRNs.

If you are exempt and have not filed this declaration, you may already have received a notice. Filing it resolves the issue.

What Changes When You Cross the INR 5 Crore Mark

When e-invoicing applies, three things change in your invoicing process:

Every qualifying invoice needs an IRN before it goes to the buyer. You cannot send the invoice and register it later. The IRN must be on the invoice.

The invoice must carry a QR code. The QR code is generated by the IRP and contains key invoice details. Tax officers can scan it offline to verify the invoice without internet access.

Your GSTR-1 gets auto-populated. Once an invoice is registered on the IRP, the data flows directly into your GSTR-1. You do not have to enter it again at filing time. Billing software that auto-populates GSTR-1 from IRP-registered invoices removes this step entirely.

Staying Ahead of the INR 5 Crore Limit

GST billing software that tracks your aggregate sales and flags when the e-invoice requirement is getting close saves you from being caught off guard mid-year. For businesses already above INR 5 crore, the right tool handles IRN generation and QR code embedding within the normal invoice creation flow. You raise the invoice, the IRN comes back from the IRP, and the QR code appears on the PDF. Your GSTR-1 is updated automatically.

FAQs

What is the e-invoice limit under GST in 2026?

The e-invoice limit under GST in 2026 is INR 5 crore in aggregate annual sales across all GST registrations under the same PAN. If your sales crossed this figure in any financial year from FY 2017-18 onwards, e-invoicing applies to you right now. The limit has not changed since August 2023.

Does e-invoicing apply if my current year sales are below INR 5 crore?

Yes, if your sales crossed INR 5 crore in any earlier year since FY 2017-18. The rule is based on past years, not just the current one. Once you cross the limit in any year, e-invoicing applies from the next financial year and does not switch off if your sales fall below later.

Does the INR 5 crore limit apply to each branch separately?

No, the INR 5 crore limit does not apply to each branch separately. Sales are calculated across all GST registrations under the same PAN. If you have branches in multiple states, their sales are combined. If the combined figure crosses INR 5 crore, all your registrations must comply.

What is the penalty for not generating an e-invoice?

The penalty for not generating an e-invoice is INR 10,000 per invoice or 100% of the tax on that invoice, whichever is higher. The invoice is also treated as invalid under GST, which means your buyer cannot claim input tax credit on it.

Is there a time limit for uploading invoices to the IRP?

For businesses with annual sales above INR 10 crore, yes: 30 days from the invoice date, effective April 1, 2025. After 30 days, the IRP rejects the upload. For businesses with sales between INR 5 crore and INR 10 crore, no formal time limit applies currently, though generating the IRN at the time of raising the invoice is best practice.