EPFO 3.0 PF Withdrawal Rules 2026: Complete Guide to Online Claims, UPI Withdrawals, Eligibility, Tax Rules and Common Mistakes

EPFO 3.0 raises auto-settlement to Rs. 5 lakh, removes employer dependency for most claims, and introduces UPI and ATM-based withdrawals. Here is everything salaried employees need to know about PF withdrawal rules in 2026.

For decades, withdrawing your Provident Fund meant paperwork, employer sign-offs, and weeks of waiting. EPFO 3.0 is changing that.

The Employees' Provident Fund Organisation's biggest digital overhaul to date covers roughly 30 crore members. It raises auto-settlement limits to Rs. 5 lakh, removes employer dependency for most claims, simplifies 13 withdrawal categories into three, and introduces UPI and ATM-based access to PF savings.

The Central Board of Trustees (CBT) approved EPFO 3.0 at its 238th meeting. The rollout is in phases through mid-2026. Some features are already live. Others are still being rolled out.

This guide is for salaried employees who want to know what has changed, first-time PF users who find the process confusing, and anyone whose PF claim was rejected.

What's New in EPFO 3.0 in 2026?

Higher auto-settlement limit

Claims up to Rs. 5 lakh are now auto-settled by the system without any human involvement, provided your UAN is fully KYC-compliant. The earlier limit was Rs. 1 lakh.

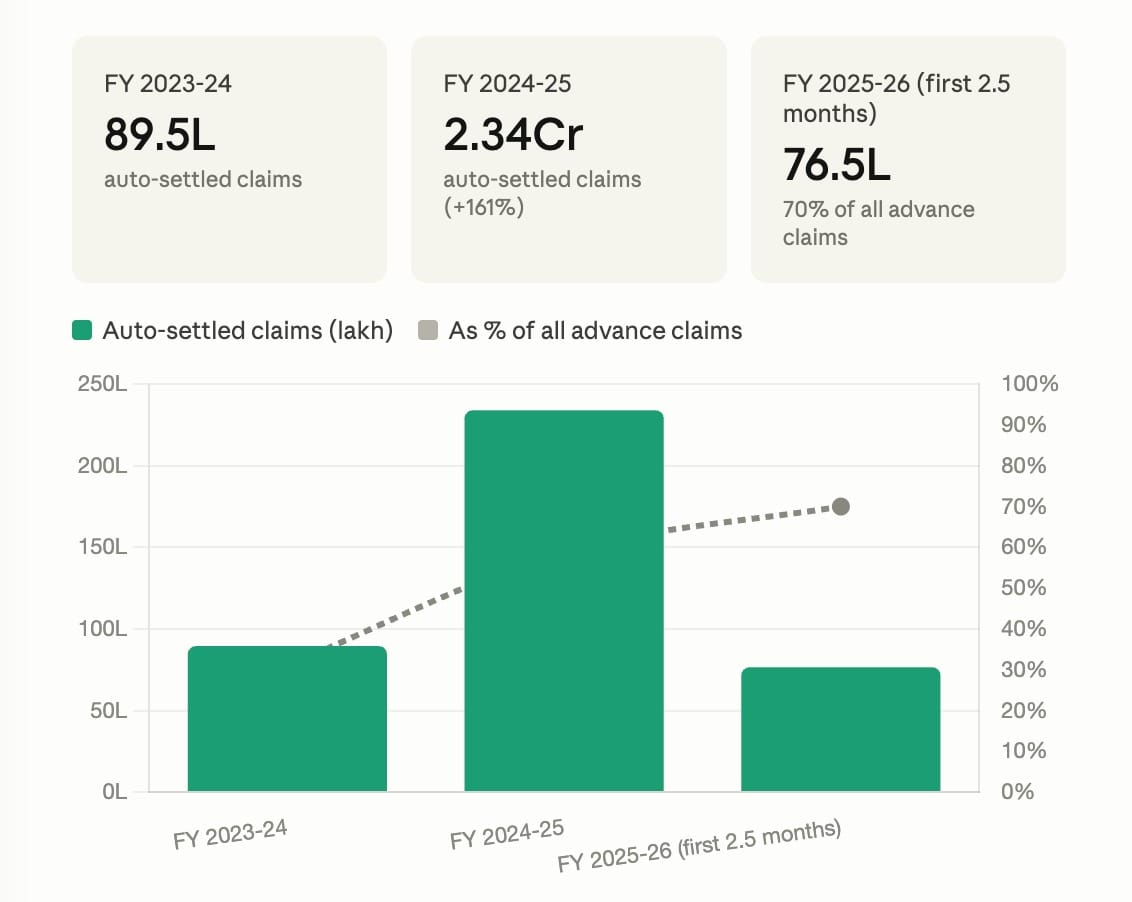

According to Union Minister Mansukh Mandaviya, EPFO processed 2.34 crore advance claims through auto-settlement in FY 2024-25, a 161% jump over the previous year. In just the first 2.5 months of FY 2025-26, 76.52 lakh claims were auto-settled, making up 70% of all advance claims.

Reduced employer dependency

If your UAN is Aadhaar-linked and KYC was previously verified by any employer, you no longer need your current employer's approval for most claims.

Three simplified withdrawal categories

The earlier 13 sub-categories have been merged into three:

- Essential Needs: Medical emergencies, marriage, and education

- Housing Needs: Home purchase, construction, loan repayment

- Special Circumstances: Natural calamities, unforeseen emergencies

Education withdrawals are now allowed up to 10 times, and marriage withdrawals up to 5 times.

UPI and ATM withdrawals (coming soon)

EPFO will allow members to withdraw eligible PF funds via UPI apps (PhonePe, Google Pay, Paytm) and via a dedicated EPFO ATM card. As of 8 June 2026, testing is complete, and the system is awaiting final regulatory clearances. No official launch date has been announced yet.

Form 121 replaces Form 15G and 15H

From 1 April 2026, the new Income Tax Act, 2025, replaced Forms 15G and 15H with a single Form 121 for TDS declarations on PF withdrawals.

EPFO 3.0: What Is Live and What Is Still Coming?

| Feature | Status | What You Should Know |

|---|---|---|

| Auto-settlement up to Rs. 5 lakh | Live | Works for fully KYC-verified UANs without any employer involvement |

| Employer-free withdrawal | Live | Aadhaar-linked UAN with prior employer-verified KYC qualifies |

| Form 121 (replaces Form 15G/15H) | Live from 1 April 2026 | EPFO circular dated 13 April 2026 confirms the transition |

| Online detail correction via OTP | Live | Name, date of birth correctable digitally in most cases |

| Simplified 3-category system | Approved, rolling out | CBT-approved; implementation underway in phases |

| EPFO ATM card | Phase-wise rollout | Cards being issued in batches through mid-2026 |

| UPI-based PF withdrawals | Testing complete, awaiting clearance | No official launch date announced as of 8 June 2026 |

PF Withdrawal Eligibility and Limits in 2026

A minimum of 25% of your total PF balance (employee contribution + employer contribution + interest) must remain in the account at all times during active service. This floor applies to all partial withdrawals, including UPI and ATM-based ones.

| Purpose | Min. Service | Max. Withdrawal | Times Allowed |

|---|---|---|---|

| Medical emergency | None | 6 months basic wages or full employee share, whichever is lower | As needed |

| Marriage | 7 years | 50% of employee contribution | Up to 5 times |

| Education | 7 years | 50% of employee contribution | Up to 10 times |

| Home purchase or construction | 5 years | 90% of total balance | Once in lifetime |

| Home loan repayment | 10 years | 90% of total balance | Once in lifetime |

| Natural calamity | None | 50% of balance or Rs. 5,000, whichever is lower | As needed |

| Unemployment (1 month) | Any | 75% of total balance | Once per unemployment spell |

| Unemployment (2+ months) | Any | 100% (full withdrawal) | Once per unemployment spell |

| Retirement (age 58+) | Any | 100% | Once |

Step-by-Step Guide: How to Withdraw PF Online in 2026

Before you begin, confirm these are in order:

- Aadhaar seeded to UAN, Aadhaar-registered mobile number active

- PAN linked to UAN (without PAN, TDS is deducted at 30%)

- Bank account number and IFSC code correct and account active

- Date of exit updated in your service history

Step 1: Log in at unifiedportal-mem.epfindia.gov.in using your UAN and password.

Step 2: Go to Manage > KYC. Confirm Aadhaar, PAN and bank account all show as Verified. Fix anything pending before proceeding.

Step 3: Click Online Services > Claim (Form-31, 19, 10C & 10D).

Step 4: Enter the last four digits of your linked bank account and verify. Tick the certificate of undertaking to proceed.

Step 5: Select the correct form.

| Form | Use for |

|---|---|

| Form 19 | Full PF settlement on resignation, unemployment or retirement |

| Form 31 | Partial advance (medical, marriage, education, housing) |

| Form 10C | Pension withdrawal or scheme certificate |

| Form 10D | Monthly pension (age 58+, 10+ years service) |

Step 6: Enter the withdrawal purpose, amount and upload supporting documents (medical certificate, marriage card, fee receipt as applicable).

Step 7: Upload Form 121 if your service is under 5 years, withdrawal exceeds Rs. 50,000, and your income is below the taxable threshold.

Step 8: Click Get Aadhaar OTP, enter the OTP and submit. Note your claim reference number.

Processing time: Auto-settled claims under Rs. 5 lakh take a few hours to 3 business days. Claims above Rs. 5 lakh take 7 to 10 working days.

Claim status: Check via the EPFO portal, UMANG app, SMS (send EPFOHO UAN ENG to 7738299899), or missed call to 011-22901406.

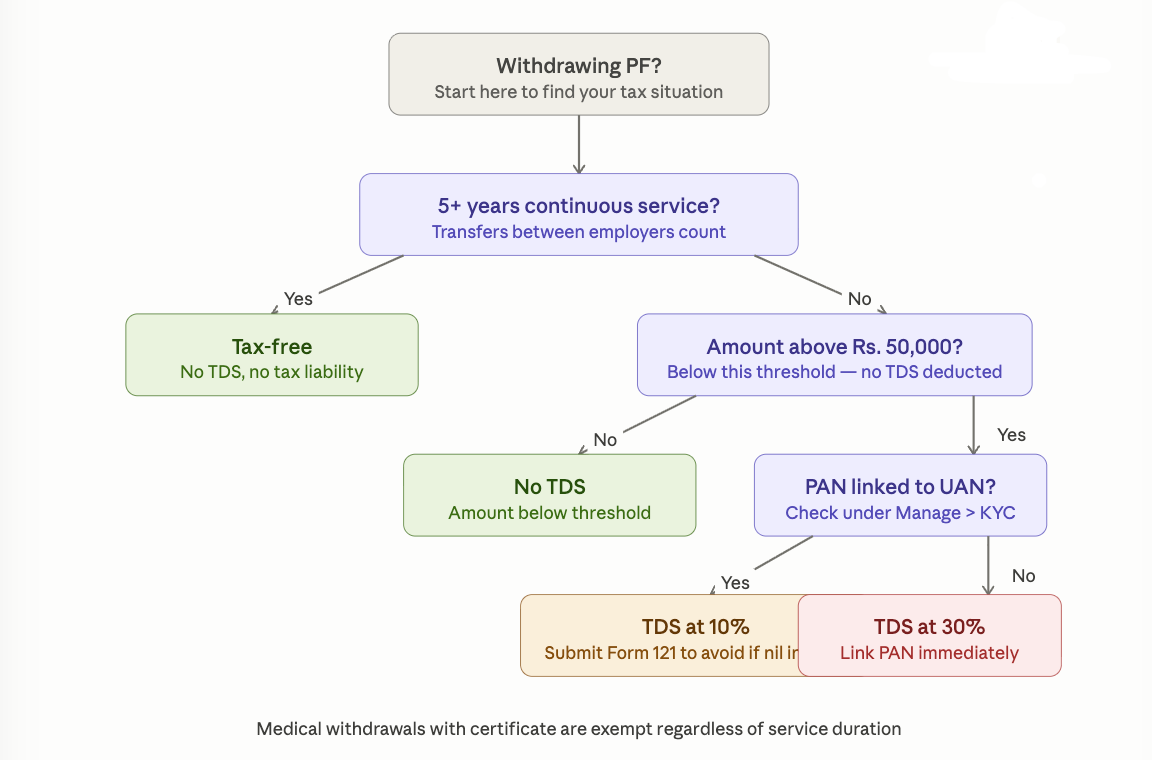

PF Withdrawal Tax Rules in 2026

| Situation | Tax Treatment |

|---|---|

| Service 5+ continuous years | Fully tax-free |

| Retirement at age 58+ | Fully tax-free |

| Medical withdrawal (with certificate) | Exempt from tax |

| PAN linked, service under 5 years, amount above Rs. 50,000 | TDS at 10% |

| PAN not linked, service under 5 years, amount above Rs. 50,000 | TDS at 30% |

Tip: Transferring PF on every job change (instead of withdrawing) keeps your 5-year continuous service count intact and keeps you tax-free on eventual withdrawal.

What is Form 121?

Form 121 is a new self-declaration introduced under the Income Tax Act, 2025, effective from 1 April 2026. It replaces the earlier Form 15G (for those under 60) and Form 15H (for senior citizens) with a single unified form.

If your total income for the year is below the taxable threshold, submit Form 121 to EPFO when filing your claim to avoid TDS altogether.

Key points:

- Submit it before your withdrawal is processed. It cannot recover TDS already deducted.

- Valid for one financial year only. Submit a fresh form each April.

- Covers both EPF withdrawal and EPS pension in a single declaration, unlike the old system.

- Claims submitted with the old Form 15G or 15H after 1 April 2026 will not be immediately rejected, but EPFO may ask for Form 121 subsequently.

Most Common Reasons PF Claims Get Rejected

| Reason | What Happens | How to Fix |

|---|---|---|

| KYC mismatch | Name, DOB or gender differs between Aadhaar and EPFO records | Submit a Joint Declaration Form through your employer |

| Wrong or inactive bank account | Incorrect IFSC, dormant account, or non-spousal joint account | Redo bank KYC; only spouse joint accounts are accepted |

| Date of exit not updated | Portal considers you still employed; full settlement forms blocked | Ask HR to update, or raise a complaint at epfigms.gov.in |

| Aadhaar not seeded to UAN | Online claims cannot proceed | Link at member portal; wait 48 hours before filing |

| Overlapping service dates | Two employers' dates overlap even by one day | EPFO's 2026 circular allows minor overlaps; reapply with clean records |

| Wrong claim form selected | Form 19 filed while still employed | Verify eligibility before selecting the form |

| Missing or blurry documents | Supporting documents incomplete or unreadable | Re-upload clear, valid documents and resubmit |

Expert Tips to Get Your Claim Approved Faster

- Sort KYC first, not last. Most rejections are KYC-related, not eligibility-related. Spend five minutes checking Aadhaar, PAN and bank details before starting the claim.

- Use the grievance portal if your employer is unresponsive. File at epfigms.gov.in to prompt faster date-of-exit updates.

- Wait 48 hours after any KYC update before filing. Recent changes may not have synced with the EPFO backend immediately.

- Submit Form 121 in April each year if your income is below the taxable limit, so it is ready before you need it.

- Transfer, do not withdraw, on every job change. This protects your 5-year service count and keeps withdrawals tax-free.

Final Thoughts

EPFO 3.0 is a genuine improvement. Auto-settlement up to Rs. 5 lakh, employer-free withdrawals for eligible members, a simplified three-category system, and the incoming UPI and ATM facilities will make PF access faster and less frustrating for crores of Indian workers.

However, UPI and ATM withdrawals are not live yet. As of 8 June 2026, testing is done, but regulatory clearances are still pending. Do not plan a withdrawal around these features until an official launch date is announced.

What to do today:

- Log in to the EPFO member portal and verify your KYC status

- Confirm your Aadhaar-registered mobile number is active

- Check your service history for overlapping dates

- Switch from Form 15G/15H to Form 121 for any future TDS declarations

Keep an eye on epfindia.gov.in and the UMANG app for the official UPI and ATM rollout date.

FAQs

Can I withdraw PF while still employed?

Yes, you can withdraw PF while still employed, but only for specific purposes: medical emergencies, marriage, education, housing or natural calamities. Full withdrawal while employed is not permitted.

Is UPI PF withdrawal available right now?

The UPI PF withdrawal is not yet available for all members. As of 8 June 2026, testing is complete, but the system is awaiting final regulatory clearances. No official launch date has been confirmed.

Can I withdraw PF without employer approval?

Yes, for most claims under Rs. 5 lakh, if your UAN is Aadhaar-linked and KYC was previously verified by any employer. Date of exit updates may still require employer action.

Is PF withdrawal taxable?

Only if you withdraw before 5 years of continuous service and the amount exceeds Rs. 50,000. After 5 years it is fully tax-free.

What if my claim is rejected?

A rejection does not mean you have lost your money. Log in, check the exact rejection reason under Track Claim Status, fix the issue and reapply.

How long does PF withdrawal take?

A few hours to 3 business days for auto-settled claims under Rs. 5 lakh. Seven to 10 working days for claims above Rs. 5 lakh.

What is the EPFO ATM card withdrawal limit?

Up to 50% of your eligible advance balance via the ATM card. The 25% floor still applies.