India’s Credit Card Spending Hits ₹23.6 Trillion in FY2026: Key Trends, Risks & RBI Changes Explained

India's credit card industry has undergone a remarkable transformation over the past five years. From fewer than 60 million cards in FY2020, the country now has over 118 million credit cards in circulation. Spending has grown from under ₹6 trillion annually to nearly ₹24 trillion in FY2026, reflecting a deep structural shift in how Indians pay for goods and services.

This report focuses on credit card data released by the Reserve Bank of India (RBI) for the period ending March 2026, with contextual comparisons to April 2025. It examines monthly spending trends, the growth of the card user base, market concentration, key growth drivers, emerging challenges, and the policy environment shaping the sector.

Understanding this data matters beyond banking. Credit card spend is a reliable proxy for private consumption, which accounts for nearly 57% of India's GDP. Shifts in card spending offer early signals about consumer confidence, retail health, and financial inclusion across income segments.

Key Highlights

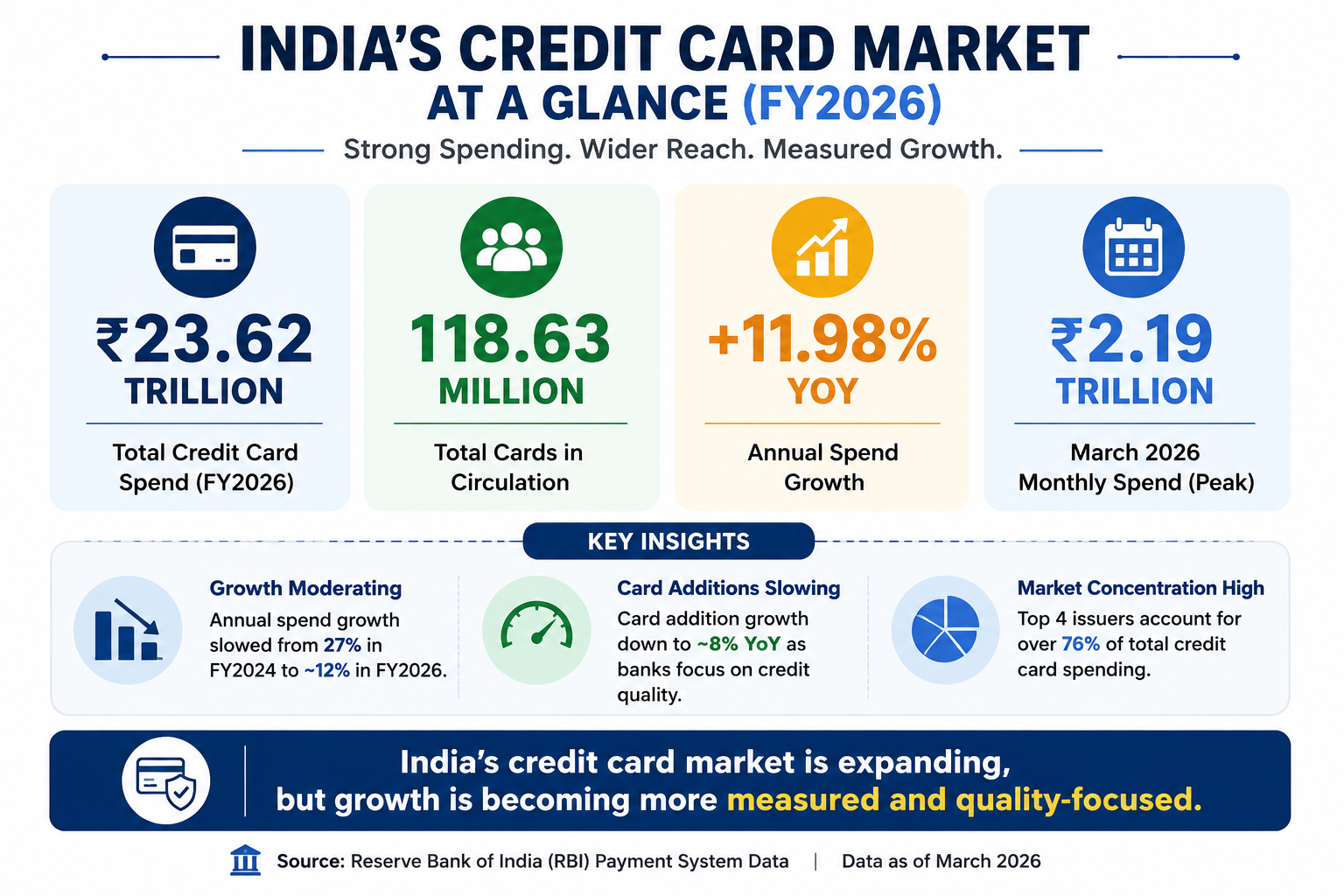

- FY2026 total credit card spend: ₹23.62 trillion, up 11.98% year-on-year from ₹21.09 trillion in FY2025

- March 2026 monthly spend: ₹2.19 trillion, a three-month high driven by year-end financial activity

- April 2025 spend (latest annual comparison point): ₹1.84 trillion, up 18% YoY from April 2024

- Total cards in circulation (March 2026): 118.63 million, up 7.96% YoY from 109.88 million

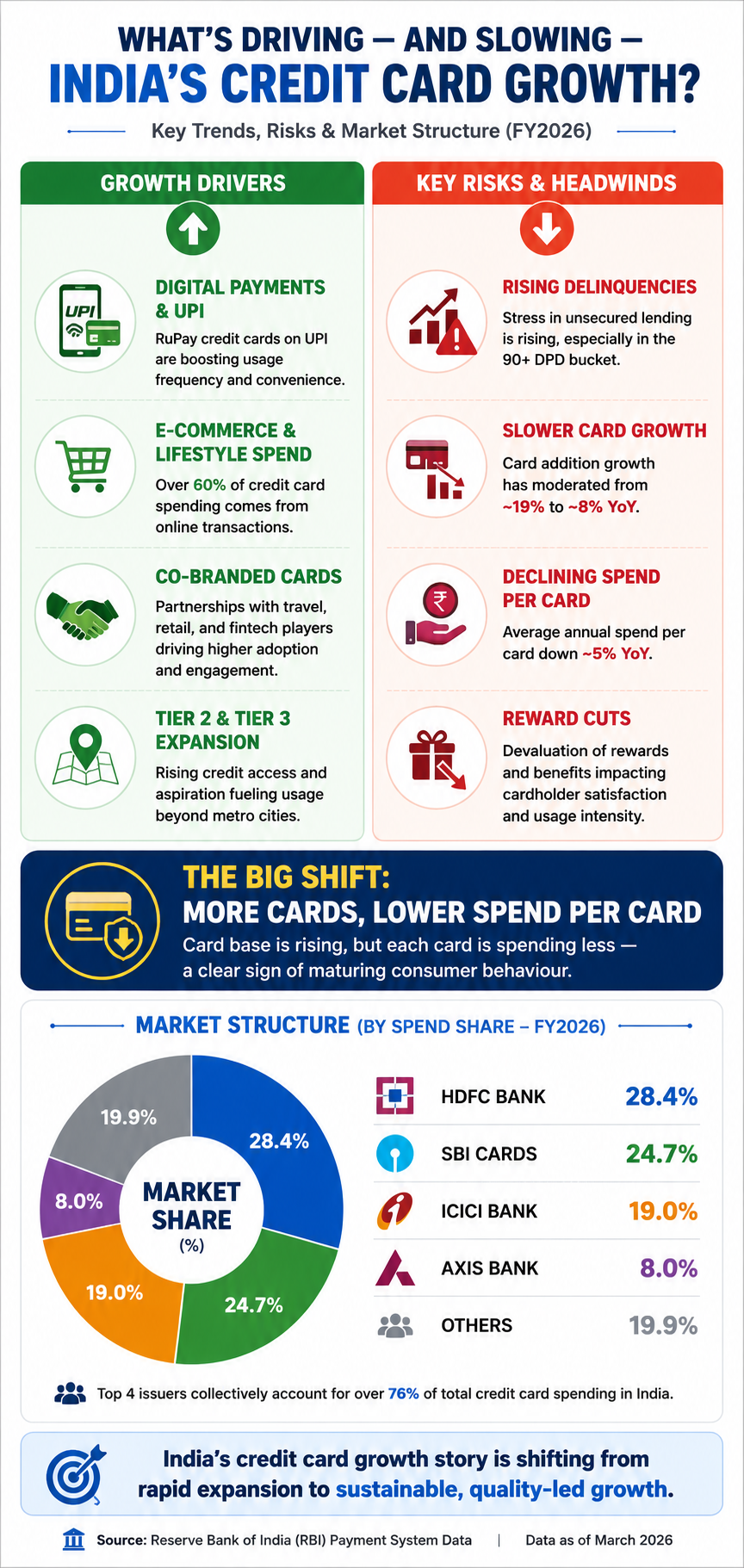

- Card additions are slowing: YoY growth of ~8% in FY26, down from ~19% in FY24, as lenders prioritise credit quality

- Growth paradox: more cards are being issued, yet average spend per card is declining, signalling cautious consumer behaviour

- Market concentration remains high: the top four banks account for over 76% of total industry spending

Monthly Spending Trend Analysis

Credit card spending in India follows a recognisable seasonal pattern. Spending peaks during the festive months of September and October, dips in January and February, and then recovers in March on the back of year-end financial settlements.

In February 2026, spending touched its lowest point in FY26 at ₹1.77 trillion. This reflected the short billing month, post-festive demand exhaustion, and cautious consumer sentiment. March 2026 saw a sharp rebound of 23.81% month-on-month to ₹2.19 trillion, driven by year-end corporate expenditures, tax-related payments, and quarterly settlements.

Recent Monthly Credit Card Spending in India (Nov 2025-Mar 2026)

| Month | Total Spend | Key Insight |

|---|---|---|

| November 2025 | ₹1.89 trillion | Post-festive moderation; down from ₹2.17T in Sept |

| December 2025 | ₹2.05 trillion | Fourth month above ₹2T threshold; festive residuals |

| January 2026 | ₹2.00 trillion | Mild cooling after year-end; YoY growth ~8% |

| February 2026 | ₹1.77 trillion | Lowest in FY26; short month and seasonal dip |

| March 2026 | ₹2.19 trillion | Three-month high; year-end financial transactions surge |

Source: Reserve Bank of India (RBI) Payment System Data

A broader pattern is evident: each time monthly spending dips sharply, as it did in February, the following month tends to rebound strongly.

Yearly Growth Overview

India's credit card spending has grown consistently over three financial years, though the pace of expansion is moderating. After the exceptional 27% growth of FY2024, partly driven by post-pandemic pent-up demand, FY2025 saw growth cool to around 15.5%. FY2026 recorded growth of nearly 12%, bringing total annual spending to ₹23.62 trillion.

This moderation is not unexpected. As the base of card spending expands, sustaining high double-digit growth becomes structurally harder. Additionally, lenders have become more conservative in card issuances following a rise in delinquencies in the unsecured lending segment during 2024-25.

Annual Credit Card Spending Comparison – FY2024 to FY2026

| Financial Year | Total Spend | YoY Growth | Key Insight |

|---|---|---|---|

| FY2024 | ₹18.26 trillion | +27% YoY | Record growth; festive surge, post-COVID rebound |

| FY2025 | ₹21.09 trillion | +15.5% YoY | Growth moderates; rising delinquencies, RBI caution |

| FY2026 | ₹23.62 trillion | +11.98% YoY | Steady growth; consumption holds, card additions slow |

Despite the slowdown in growth rate, the absolute volumes remain robust. Monthly spending crossed ₹2 trillion on four separate occasions in 2025-26, a milestone that was rarely achieved in earlier years.

Credit Card User Base Growth

India's credit card base stood at 118.63 million as of March 2026, up from 109.88 million a year earlier. This marks a YoY growth of approximately 7.96%, a significant deceleration from the 19% YoY growth recorded in March 2024.

The slowdown in card additions reflects a deliberate shift in strategy by major lenders. Following elevated defaults and stress in unsecured portfolios, banks moved from aggressive customer acquisition to cross-selling cards to existing, creditworthy customers. Net card additions in March 2026 stood at approximately 930,000, a figure consistent with the more measured pace seen throughout FY26.

Key Drivers of Growth

- Rising smartphone penetration and digital literacy, particularly among younger, urban consumers

- Integration of RuPay credit cards with UPI, enabling credit card usage for small-ticket QR-code transactions

- Growth of co-branded cards with travel, e-commerce, and lifestyle brands that attract aspirational spenders

- Government-led push for digital payments under the Digital India initiative

Despite surpassing 118 million cards, India's credit card penetration remains modest at under 10% of the adult population, indicating substantial headroom for long-term growth.

Market Share and Key Players

India's credit card market is heavily concentrated. The four largest issuers, HDFC Bank, SBI Cards, ICICI Bank, and Axis Bank, collectively account for over 76% of total industry spending. This concentration has remained stable despite the entry of newer players.

Market Share Overview - Leading Credit Card Issuers (March 2026)

| Bank / Issuer | Cards in Force (Mar-26) | Approx. Spend Share | Key Note |

|---|---|---|---|

| HDFC Bank | 26.31 million | ~28.4% | Market leader; 10.37% YoY card growth |

| SBI Cards | 22.10 million | ~24.7% | Biggest gainer in spend share over FY26 |

| ICICI Bank | 19.05 million | ~19% | Steady growth; 4.62% YoY card rise |

| Axis Bank | 16.03 million | ~8% | Moderate growth; focusing on quality over volume |

| Others | ~35 million | ~19.9% | Smaller banks, fintechs, co-branded issuers |

HDFC Bank remains the undisputed leader with 26.31 million cards and a spending share of approximately 28.4%. Notably, SBI Cards has been the biggest gainer in spend share through FY26, rising from 19.3% in April 2025 to 24.7% by January 2026.

Mid-sized banks such as Federal Bank and Yes Bank have shown modest growth, but their base remains small. The top 10 banks collectively hold a 93% share of spending, leaving very little room for smaller players.

Key Growth Drivers

Several structural forces continue to push credit card adoption and spending higher:

Digital Payments and UPI Integration

Digital payments now account for nearly 99.8% of all transactions in India by volume. The integration of credit cards into UPI flows, particularly through RuPay credit cards, has expanded the utility of credit cards to everyday low-ticket purchases. Cards linked to the UPI register up to eight times higher transaction frequency than traditional usage.

E-Commerce and Lifestyle Spending

Online transactions account for over 60% of credit card spending by value. E-commerce, food delivery, travel bookings, streaming subscriptions, and entertainment drive a significant share of card transactions. Premium lifestyle and travel cards have seen strong uptake among urban professionals.

Co-Branded and Fintech Cards

Co-branded cards offered in partnership with airlines, hotel chains, retail brands, and food-delivery platforms have widened the addressable market. Fintech firms have further lowered onboarding barriers by enabling instant digital card issuance through mobile applications, making credit accessible to younger, first-time borrowers.

Tier 2 and Tier 3 City Expansion

Credit card adoption is no longer limited to metropolitan areas. Young professionals in smaller cities increasingly use cards for lifestyle, travel, and online shopping. This geographic broadening is one of the most significant structural trends underpinning the industry's long-term prospects.

Challenges and Concerns

Despite the broadly positive growth, several risks and headwinds deserve attention:

- Slowing growth rate: FY26's 12% YoY growth, while healthy, marks a continued deceleration from the 27% highs of FY24. If consumption weakens, this number could fall further.

- Rising delinquencies: Elevated stress in unsecured lending portfolios has prompted lenders to become cautious. Card addition growth fell from 19% in FY24 to around 8% in FY26, and credit quality remains a central concern.

- Declining average spend per card: In January 2026, average spend per card dropped 3.5% month-on-month to approximately ₹17,060. Average spend per transaction also fell 13% YoY, suggesting consumers are making more transactions of smaller value rather than high-ticket purchases.

- Reward dilution: Several leading banks have cut reward rates and lounge access benefits on mid-tier cards to manage profitability pressure. This may reduce the appeal of card usage among value-conscious consumers.

- Growth paradox: Banks are issuing more cards, but many new cards appear to be going to existing cardholders who spread spending across multiple products rather than increasing their total consumption.

Regulatory and Policy Changes (2026)

The regulatory landscape governing credit cards in India has evolved meaningfully in 2026, with several key changes taking effect from April 1, 2026:

- Two-factor authentication mandate: The RBI now requires every digital payment, including credit card transactions, to use at least two independent authentication factors, with at least one being dynamically generated for that specific transaction. This increases transaction security but may add a small layer of friction for users.

- International card-not-present transactions: The RBI plans to extend similar two-factor authentication norms to international card-not-present transactions by October 2026, which will impact online cross-border purchases.

- Enhanced income-linked spend reporting: Under the new Income Tax Act (2025), credit card spending above ₹10 lakh annually is subject to mandatory reporting to the Income Tax Department via the Statement of Financial Transactions (SFT) framework. This is a reporting mechanism, not a new tax, but greater scrutiny may moderate discretionary spending among some users.

- Faster credit reporting: From April 2026, payment updates, whether timely or missed, must reflect in credit reports within 7 to 14 days rather than the earlier 15 to 30 days. This tightens accountability for borrowers and gives lenders more timely risk data.

Collectively, these changes are expected to improve system transparency and reduce fraud, though they also add compliance costs for issuers and may modestly slow new card adoption as banks conduct tighter credit checks.

Future Outlook

The near-term outlook remains cautiously positive. Spending is expected to stay stable in FY27, supported by private consumption and digital adoption. However, card additions may remain limited as lenders prioritise credit quality.

Long-Term Growth Indicators

- Market projected to grow from USD 20.1 billion (2025) to USD 38.3 billion by 2034 (CAGR 7.41%)

- Low penetration (under 10%) indicates strong headroom

- UPI-credit card linkage offers a new growth channel

- Premium card segments expected to expand

The key question is whether growth will reaccelerate to 15–18% or stabilise in the 8-12% range.

Conclusion

India's credit card market closes FY2026 in reasonable health. Annual spending of ₹23.62 trillion, a card base of 118.63 million, and strong monthly peaks reflect a maturing ecosystem.

However, growth is slowing, average spend per card is declining, and lenders are more cautious. The market is expanding geographically, but usage intensity is not rising proportionately.

The industry is now transitioning from a volume-led phase to a quality-led phase. Future growth will depend on responsible credit expansion, effective product usage, and deeper penetration beyond metropolitan centres.