Post-DPDP Act World: Why consent, privacy, and compliance matter in debt recovery

This article has been contributed by Ananth Shroff, Founder & CEO, DPDzero

For decades, debt collection in India has been viewed as one of the least consumer-friendly sectors in financial services. The very mention of "collections" conjures up images of endless calls, harsh reminders, and opaque recovery practices. But in 2023, the landscape changed dramatically with the introduction of India’s Digital Personal Data Protection (DPDP) Act, a law that redefined how personal data must be collected, processed, and protected.

This Act is not just about “data privacy.” It is about a mindset shift from authority to accountability, from compliance to consent. And nowhere is this transformation more urgent and necessary than in the debt recovery ecosystem, where sensitive personal and financial data is handled by lenders, agencies, and technology partners on a daily basis.

As someone leading a company at the intersection of technology, lending, and collections, I see the DPDP Act not as a compliance hurdle, but as a strategic opportunity to rebuild trust in the debt ecosystem.

Traditionally, debt collection operated in a regulatory vacuum when it came to data handling. Contact information was often shared across multiple intermediaries: agents, call centers, and fintech partners with minimal oversight or consent tracking. Borrowers, meanwhile, rarely knew who had access to their personal details or how their data was being used.

While financial institutions were governed by frameworks like the RBI’s Fair Practices Code, there was no singular law outlining the rights of individuals over their personal data. As a result, privacy was often collateral damage in the race to recover dues quickly.

This is precisely where the DPDP Act becomes a watershed moment.

The DPDP Shift: From Obligation to Empowerment

The DPDP Act changes the game by codifying privacy as a fundamental right and setting clear expectations for how businesses, whether banks, NBFCs, or collection agencies, must handle personal data. Under the new regime, every piece of borrower data, contact details, credit information, location, and communication records is considered personal data, and thus subject to strict conditions of collection, storage, and use. Key tenets like lawful purpose, data minimization, storage limitation, and most importantly, explicit consent, are now non-negotiable.

For debt recovery, this translates to three major responsibilities for Data Fiduciary and Data Processor:

- Collect only what is necessary: A collector no longer needs to know every detail about a borrower’s financial life, just enough to execute their part of the process.

- Obtain and respect consent: Consent must be freely given, informed, specific, and revocable. The borrower should know why their data is being shared, with whom, and for how long.

- Ensure accountability across the data chain: Every intermediary, whether an outsourced agency or a tech partner, is now answerable for how they handle the data.

This framework isn’t just a regulatory obligation; it’s the foundation for rebuilding borrower trust.

Debt Collection Meets Data Protection: A Necessary Evolution

We’ve always believed that collections done right are about empathy and experience, not enforcement. The DPDP Act strengthens our inherent philosophy and ethos behind building DPDzero.

Here’s how privacy, consent, and compliance directly impact debt recovery in the post-DPDP world:

- Consent is the new currency of credibility: A borrower who has fallen behind on payments is already in a vulnerable position. When they see that the communication they receive is consent-based, transparent, and respectful, they’re far more likely to engage constructively.

A consent-driven approach signals that the lender values the borrower’s autonomy and dignity. Over time, this builds a feedback loop of trust, one where borrowers are more willing to talk, negotiate, and settle dues.

- Data privacy safeguards brand reputation: For lending institutions (including Banks, NBFCs or FinTechs), a data breach or misuse incident in the collections process can be devastating not just in penalties, but in public trust.

By adopting DPDP-compliant data management, secure storage, access logs, encryption, and deletion protocols, companies protect not only their customers’ data but also their own reputation. In a digital-first world, brand equity and data ethics go hand in hand.

- Compliance can be a competitive advantage: Early adopters of strong compliance frameworks will stand apart. They will be the partners of choice for banks and NBFCs who are under increasing scrutiny to ensure their third-party vendors adhere to DPDP norms.

For example, at DPDzero, we’ve embedded consent workflows, data encryption, and automated anonymization into our core technology stack. This means lenders can trust that borrower data is never misused, and borrowers can be confident that their privacy is protected throughout the collections cycle.

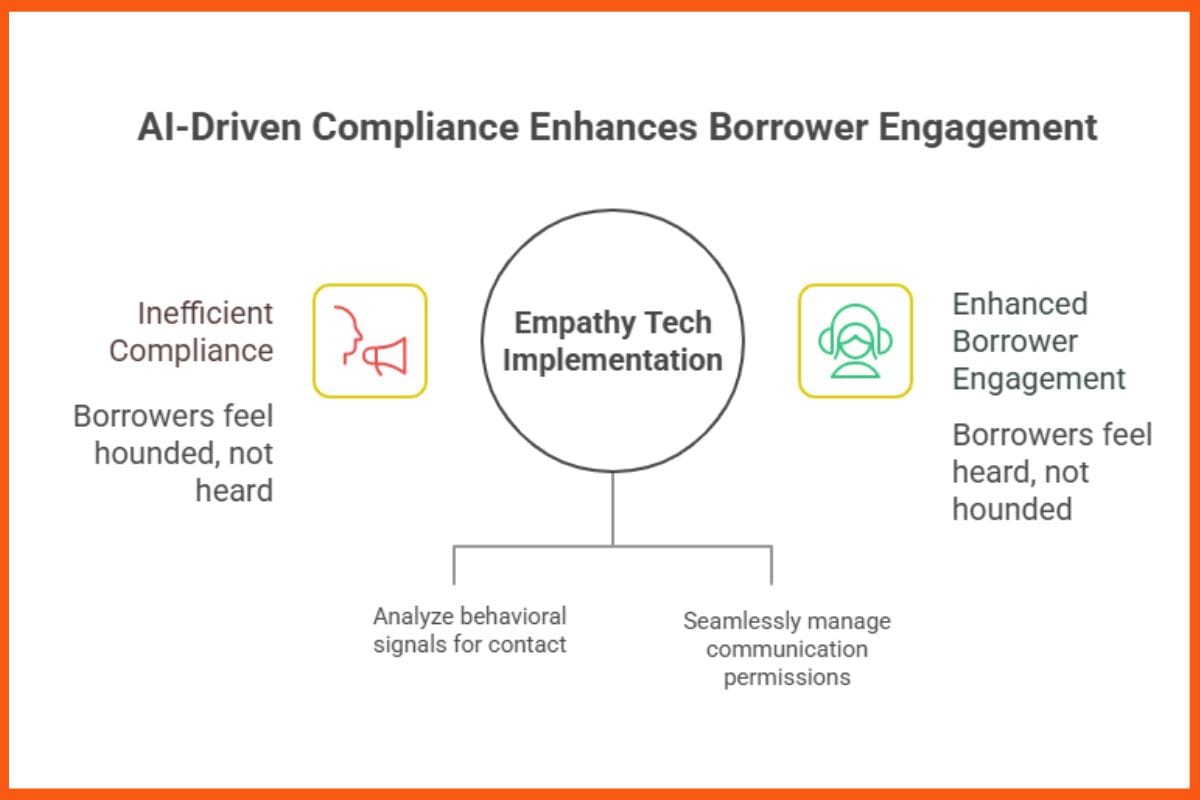

The rise of “Empathy Tech” in Debt Recovery

Technology is playing a pivotal role in turning compliance into capability. AI-driven platforms like ours can now handle millions of borrower interactions over SMS, WhatsApp, calls, and emails, while ensuring every step is consent-tracked and privacy-protected.

For instance, AI can analyze behavioral signals to determine when and how a borrower prefers to be contacted, ensuring relevance instead of repetition. Digital consent layers can be built into every communication flow, allowing borrowers to opt in, pause, or revoke permissions seamlessly.

This new wave of “empathy tech” ensures that compliance doesn’t come at the cost of efficiency. Instead, it enhances engagement by making borrowers feel heard, not hounded.

Building the Future of Responsible Collections

The DPDP Act is not a one-time compliance checklist, it’s the foundation of a new social contract between lenders, borrowers, and technology providers.

Debt recovery companies must evolve from being agents of collection to stewards of trust. That means investing in:

- Robust consent management systems

- Transparent borrower communication

- Regular privacy audits and training

- Ethical AI models that prioritize borrower welfare alongside recovery rates

Ultimately, debt recovery is about restoring financial discipline, not imposing it. And in a data-protected world, that restoration can only happen when borrowers trust the process.

Compliance is Just Good Business Sense

The DPDP Act is a landmark moment for India’s digital economy. For debt collection, it marks the end of aggressive, opaque practices and the beginning of an era where privacy, consent, and compliance become drivers of better outcomes.

At DPDzero, we’ve seen firsthand that when technology respects privacy and communication is grounded in empathy, collections become more efficient, not less. Borrowers respond positively when they feel respected.

The future of debt recovery belongs to companies that don’t just comply with the DPDP Act but champion its intent: to empower individuals, protect their data, and build a more humane financial ecosystem.

In the end, compliance isn’t just the right thing to do, it’s the smartest business strategy for shaping the future of financial services in India and beyond.