Section 269ST of the Income Tax Act: Cash Payment Limit Explained (2026)

Section 269ST says no person can receive INR 2 lakh or more in cash from one person in a day, for one transaction, or for one event. The penalty is 100% of the cash received, and it falls on the receiver, not the payer. Three triggers, real examples, and what businesses most commonly get wrong.

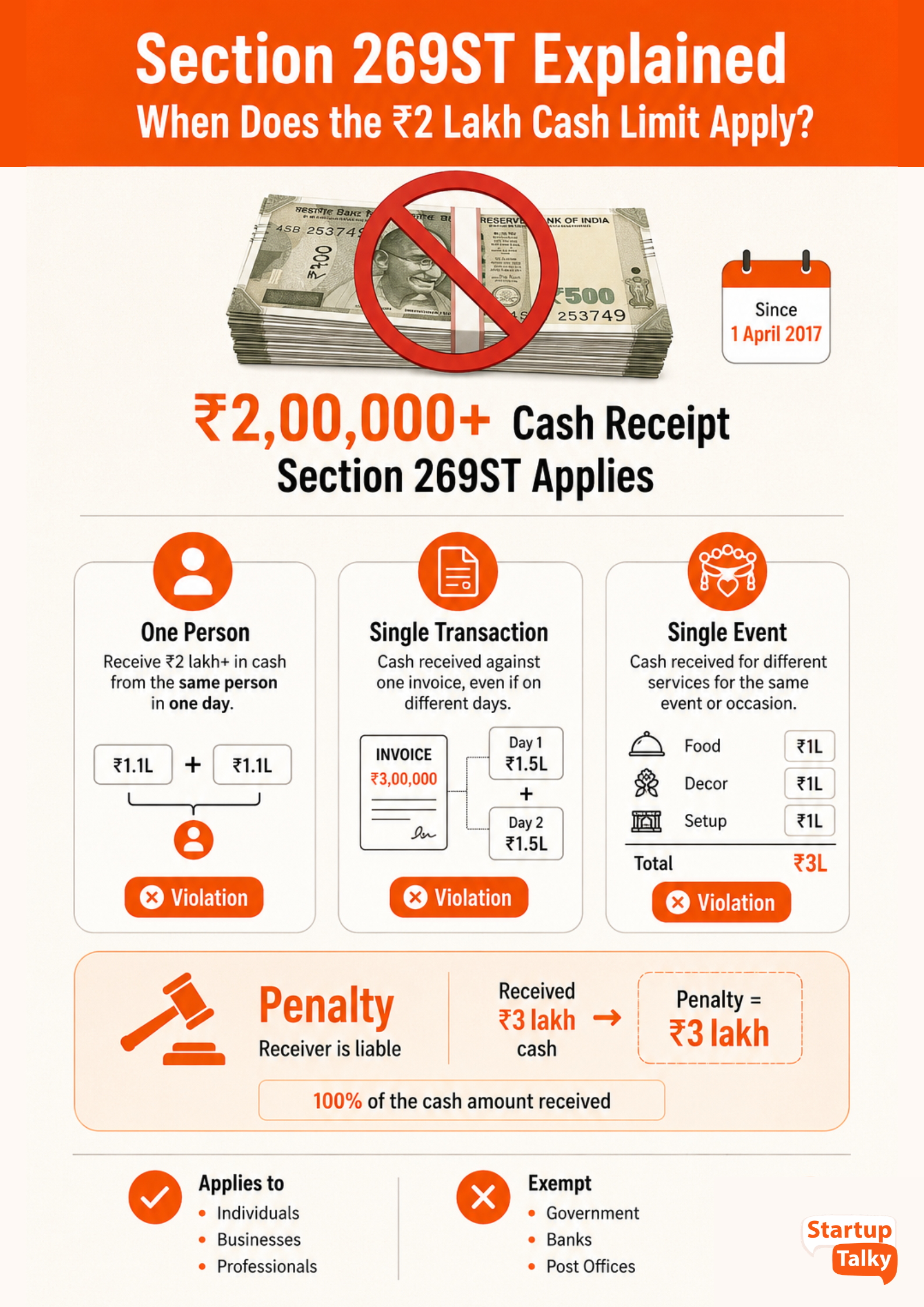

Section 269ST of the Income Tax Act says no person can receive INR 2 lakh or more in cash from a single person in a day, against a single transaction, or for a single event or occasion. The rule has been in place since April 1, 2017. The limit has not changed.

If you cross the limit, the penalty is equal to the full cash amount received. Not a percentage of it. The entire amount. And the penalty falls on the person who receives the cash, not the person who pays it.

If you want to track and block cash receipts above INR 2 lakh automatically from your invoicing software, BillForge does this at the invoice level, so you never accept a non-compliant payment by mistake.

What Exactly Does Section 269ST Say?

Section 269ST is the cash transaction limit in the Indian income tax law. No person can receive INR 2 lakh or more in cash from a single person in a day, for a single transaction, or for a single event or occasion. This applies to every individual, business, and entity in India, regardless of size or sector. Introduced on April 1, 2017, the INR 2 lakh cash limit has not changed since.

1. From a single person in a single day: If you receive INR 1.1 lakh in the morning and INR 1.1 lakh in the evening from the same person, that is INR 2.2 lakh in a day from one person. Section 269ST is violated even though neither individual payment crossed INR 2 lakh.

2. Against a single transaction: If you sell goods worth INR 3 lakh on one invoice and the buyer pays INR 1.5 lakh in cash today and INR 1.5 lakh in cash tomorrow, that is one transaction split across two days. Section 269ST is still violated because the total cash against that single invoice exceeds INR 2 lakh.

3. For a single event or occasion: If you are a caterer and one client pays you INR 1 lakh for food, INR 1 lakh for decoration, and INR 1 lakh for setup, all for the same wedding, the total is INR 3 lakh from one person for one occasion. Section 269ST is violated even though the payments were for different services and possibly on different dates.

The third trigger is the widest, and the one most businesses overlook. It does not matter how you break up the billing. If the services relate to a single event or occasion and the total cash from that person crosses INR 2 lakh, the rule applies.

Who Does This Apply To?

Section 269ST applies to every person in India: individuals, sole proprietors, partnership firms, private limited companies, LLPs, trusts, and all other entities. There is no turnover limit. A freelancer earning INR 5 lakh a year and a company with INR 500 crore revenue are both covered equally. Resident and non-resident alike.

The only people exempt are:

- Government bodies (central, state, and local)

- Banking companies (including co-operative banks)

- Post office savings banks

- Any person or class of persons specifically notified by the central government

This means hospitals, event planners, jewellers, car dealers, landlords, lawyers, and every other business that handles large cash payments must comply.

The Penalty: Who Pays and How Much

The section 269ST penalty under Section 271DA falls on the person who receives the cash, not the person who pays it. This is important. Even if a customer insists on paying in cash, accepting it makes you liable.

The penalty amount equals the full cash amount received in violation. If you accept INR 3 lakh in cash against one invoice, the penalty is INR 3 lakh. This is a 100% penalty, not a percentage. There is no lower limit.

The penalty can only be imposed by a Joint Commissioner of Income Tax, not an assessing officer. It can be waived if you can prove there were good and sufficient reasons for the violation. The law does not define what qualifies, which means this is decided on a case-by-case basis.

The Three Triggers Explained With Examples

Example 1: Single day, same person

Ram sells furniture worth INR 4.5 lakh to one customer through three different invoices of INR 1.5 lakh each. The customer pays all three in cash on the same day. Total cash from one person in one day: INR 4.5 lakh. Section 269ST is violated even though each invoice was below INR 2 lakh.

Example 2: Single transaction, multiple days

Priya provides website development services for INR 2.5 lakh under one contract. The client pays INR 1.2 lakh in cash on Day 1 and INR 1.3 lakh in cash on Day 5. This is one transaction (one contract) and the total cash received is INR 2.5 lakh. Section 269ST is violated.

Example 3: Single occasion

Suresh handles catering, decoration, and transport for one wedding. He receives INR 1 lakh cash for catering, INR 1.5 lakh cash for decoration, and INR 80,000 cash for transport from the same person on different dates. Total cash for one occasion from one person: INR 3.3 lakh. Section 269ST is violated even though no single payment crossed INR 2 lakh.

What Counts as an Acceptable Mode of Payment?

For amounts above INR 2 lakh, any payment through banking or digital channels is acceptable. Account payee cheque, bank draft, NEFT, RTGS, IMPS, UPI, BHIM, Aadhaar Pay, debit card, credit card, and net banking all qualify. Cash does not, regardless of the reason. Cash withdrawals from a bank or post office by the account holder are not restricted.

Common Situations Where This Catches Businesses Off Guard

Some of the situations where Section 269ST of the Income Tax Act catches businesses include:

- Real estate: Almost all property transactions exceed INR 2 lakh. Accepting any cash for a property sale is effectively prohibited. In April 2025, the Supreme Court directed all courts and sub-registrar offices to report cash transactions of INR 2 lakh or more in property dealings to the jurisdictional income tax officer.

- Events and weddings: Caterers, decorators, venues, and photographers dealing with one client for one event must be careful about the occasion-based trigger. The total cash from one person for one event is what matters, not individual service bills.

- Car dealers: A customer buying a car worth INR 5 lakh and paying INR 2.5 lakh in cash violates the rule on that single transaction.

- Medical services: Hospitals and clinics are not exempt from Section 269ST. A patient paying INR 2 lakh or more for surgery or treatment in cash puts the hospital at risk of penalty. During the COVID second wave in April-May 2021, CBDT provided a temporary relaxation for hospitals and treatment centres, which has since expired.

- Freelancers and consultants: If a client pays you INR 2 lakh or more in cash for professional services, the limit applies to you as the receiver. For freelancers working with multiple clients, understanding how to invoice clients and track payments correctly prevents accidental violations.

- Jewellers: High-value jewellery purchases in cash are a common trigger. Each cash receipt above INR 2 lakh from one customer in one day for jewellery is covered.

Loan Repayments to NBFCs and HFCs

One clarification the income tax department issued specifically addresses loan repayments to non-banking finance companies and housing finance companies. Each loan instalment is treated as a separate transaction. Instalments are not clubbed together. So if your EMI is INR 50,000 a month, you can pay it in cash (though it is still better practice to use banking channels). But if a single EMI is INR 2 lakh or more, that instalment cannot be paid in cash.

Section 269ST vs Section 269SS: What Is the Difference?

Both sections restrict cash transactions, but they cover different situations. The cash transaction limit under 269ST is INR 2 lakh for any receipt. Section 269SS covers a lower limit of INR 20,000 specifically for loans and deposits.

The practical difference: if someone gives you a cash loan of INR 25,000, Section 269SS applies. If someone pays you INR 2 lakh in cash for services, Section 269ST applies.

Section 269ST and Gifts from Relatives

Cash gifts between relatives are tax-exempt under the Income Tax Act, but that exemption does not override Section 269ST. If a relative gives you INR 3 lakh in cash as a gift, you are receiving INR 3 lakh in cash from one person on one occasion. Section 269ST applies.

This surprises many families at weddings and festivals where large cash gifts are common. The person receiving the cash is liable for the penalty.

Does Section 269ST Apply to Agricultural Income?

Yes. Section 269ST applies to everyone, including farmers and agricultural traders. The only exemptions are government bodies, banks, and post offices. Agricultural cash receipts of INR 2 lakh or more from a single buyer in a day are covered.

How Tax Authorities Discover Violations

The income tax department tracks high-value cash transactions through:

- Form 61A (Statement of Financial Transactions), which banks, registrars, and other specified entities file with the department

- Tax audits under Section 44AB, where auditors are required to report transactions above the limits under Sections 269SS and 269ST

- Sub-registrar reports on property cash transactions following the Supreme Court's April 2025 direction

- Third-party information from banks and payment platforms

GST-registered businesses face additional scrutiny because their invoice data is visible through GSTR-1 returns. A cash receipt that does not match the invoiced amount, or a large cash receipt that does not appear in bank statements, is a common audit trigger. Businesses issuing GST-compliant invoices with proper records have a complete audit trail if questioned.

FAQs

What is Section 269ST of the Income Tax Act?

Section 269ST prohibits any person from receiving INR 2 lakh or more in cash from a single person in a day, for a single transaction, or for a single event or occasion. It applies to all individuals and entities in India except government bodies, banks, and post offices. Introduced in 2017, the limit has not changed.

What is the penalty for violating Section 269ST?

The penalty under Section 271DA equals the full cash amount received in violation. If you receive INR 3 lakh in cash against one invoice, the penalty is INR 3 lakh. The penalty falls on the receiver, not the payer. It can be waived if good and sufficient reasons are proved, but the law does not define what qualifies.

Can you split a cash payment to avoid Section 269ST?

No. Splitting a payment across multiple invoices to the same person on the same day, across multiple dates for the same transaction, or across multiple services for the same event does not help. All three scenarios are specifically covered by the three triggers in Section 269ST.

Does Section 269ST apply to gifts received in cash from relatives?

Yes. The exemption for tax-free gifts from relatives under the Income Tax Act does not override Section 269ST. Receiving INR 2 lakh or more in cash from a relative is still a violation.

Is cash from agricultural sales covered under Section 269ST?

Yes. Farmers and agricultural traders are covered. The INR 2 lakh limit applies to all cash receipts from a single person in a day, regardless of whether the income is agricultural.

What is the difference between Section 269SS and Section 269ST

Section 269SS restricts taking loans or deposits in cash above INR 20,000. Section 269ST restricts receiving any payment in cash of INR 2 lakh or more from a single person for any reason. Both fall on the receiver. Transactions covered by 269SS are excluded from 269ST.